Vietnam’s cashew sector has opened 2026 with the kind of January that demands attention. The latest VINACAS figures show an industry firing on all cylinders: kernel exports surged over 42% year-on-year, raw nut imports jumped 36%, and the entire supply chain appears to be running at full capacity.

But the headline numbers conceal a story that is more nuanced than a simple growth narrative. Import prices for raw nuts are falling even as volumes rise. The sourcing map looks very different from a year ago, with Tanzania dominating January’s supply picture as the only major origin with fresh crop available this time of year, while Cambodia’s off-season means its contribution is negligible until the harvest begins in the coming weeks. And kernel export prices remain essentially flat year-on-year, meaning processors are moving far more product without earning significantly more per ton.

January’s data captures a specific seasonal moment: the window between harvests, when African supply dominates and Cambodia is quiet. What it shows is an industry that knows how to keep the machine running, even when its largest structural supplier is temporarily absent.

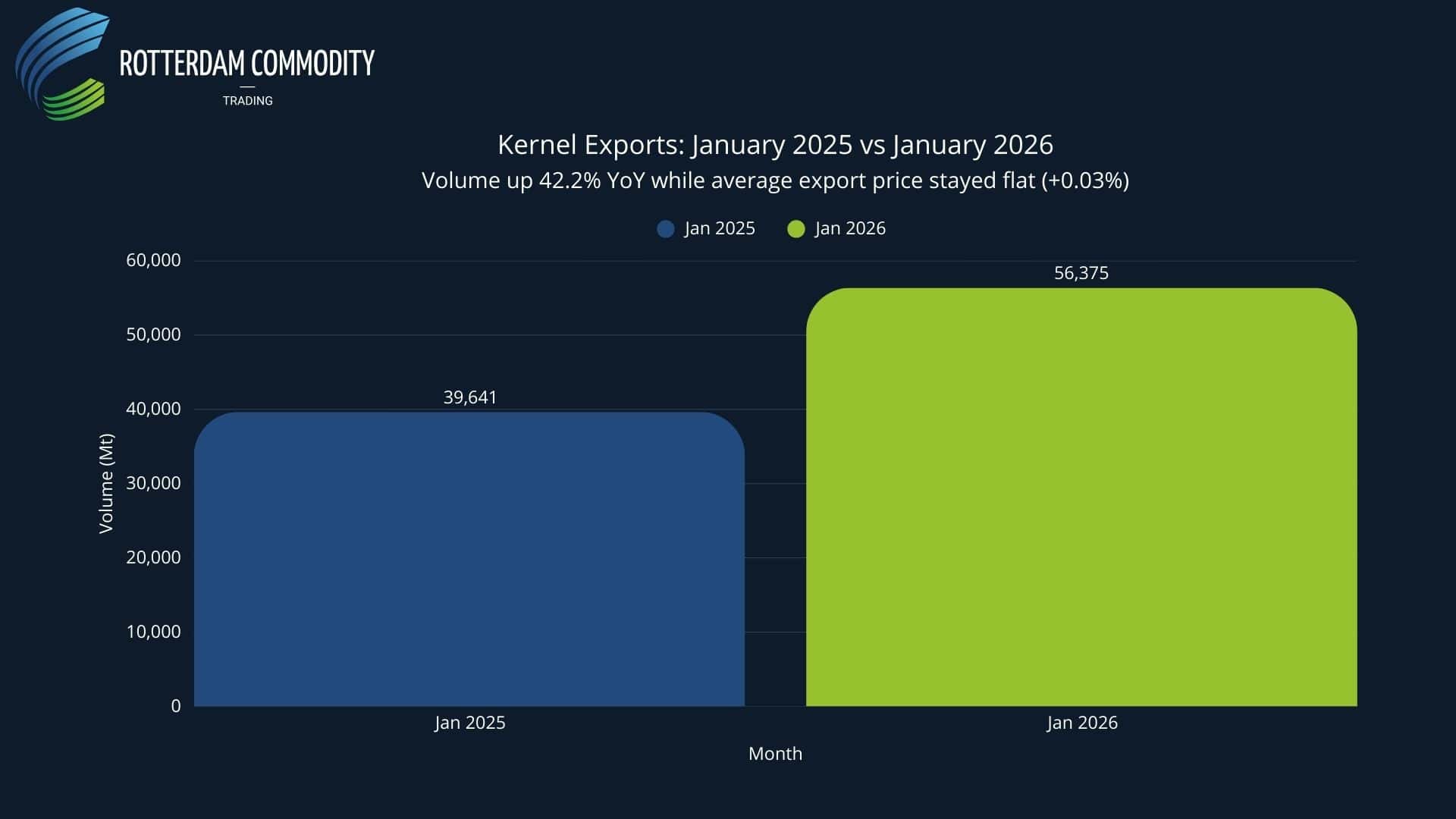

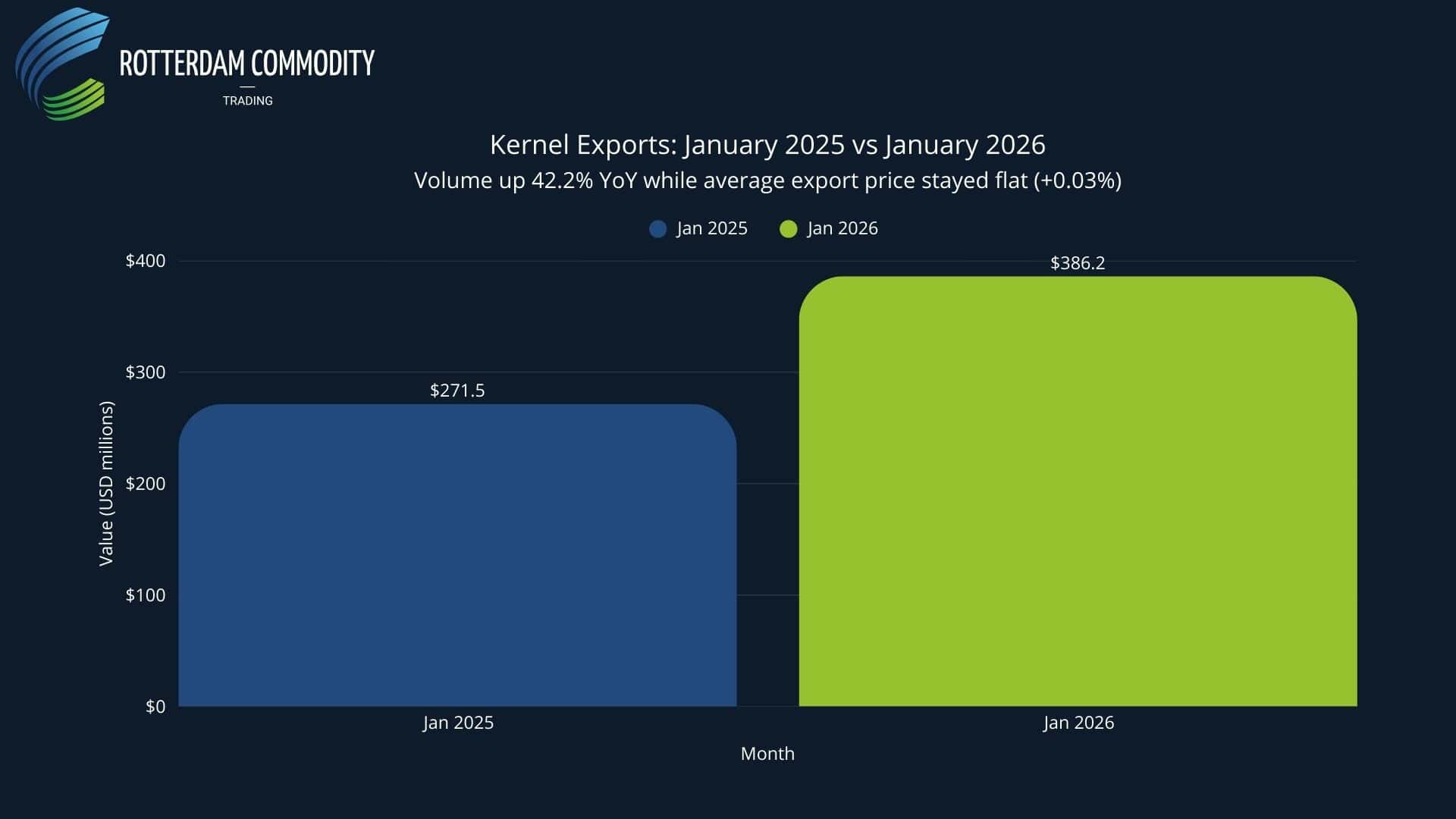

Kernel Exports: Volume Explodes, but Where’s the Margin?

Vietnam exported 56,375 metric tons of semi-processed cashew kernels in January 2026, a remarkable 42.2% increase over January 2025. Export turnover grew in near-perfect lockstep at 42.3%, reaching USD 386.2 million.

The average export price landed at USD 6,850 per ton, virtually unchanged from a year ago (+0.03%). This is the critical signal: processors are shipping dramatically more product, but the price per ton has not moved. In a year where input costs remain elevated, this means the margin equation is being resolved through volume, not through pricing power.

The benchmark WW320 grade traded between USD 3.14 and USD 4.19 per pound FOB Vietnam in January, averaging around USD 3.67/lb, up 10.1% year-on-year. The spread between the highest and lowest FOB price recorded in the month was a notable USD 1.05/lb, reflecting the wide quality and contract diversity among Vietnamese exporters. VINACAS notes that FDI-linked processors tend to report at the lower end of this range.

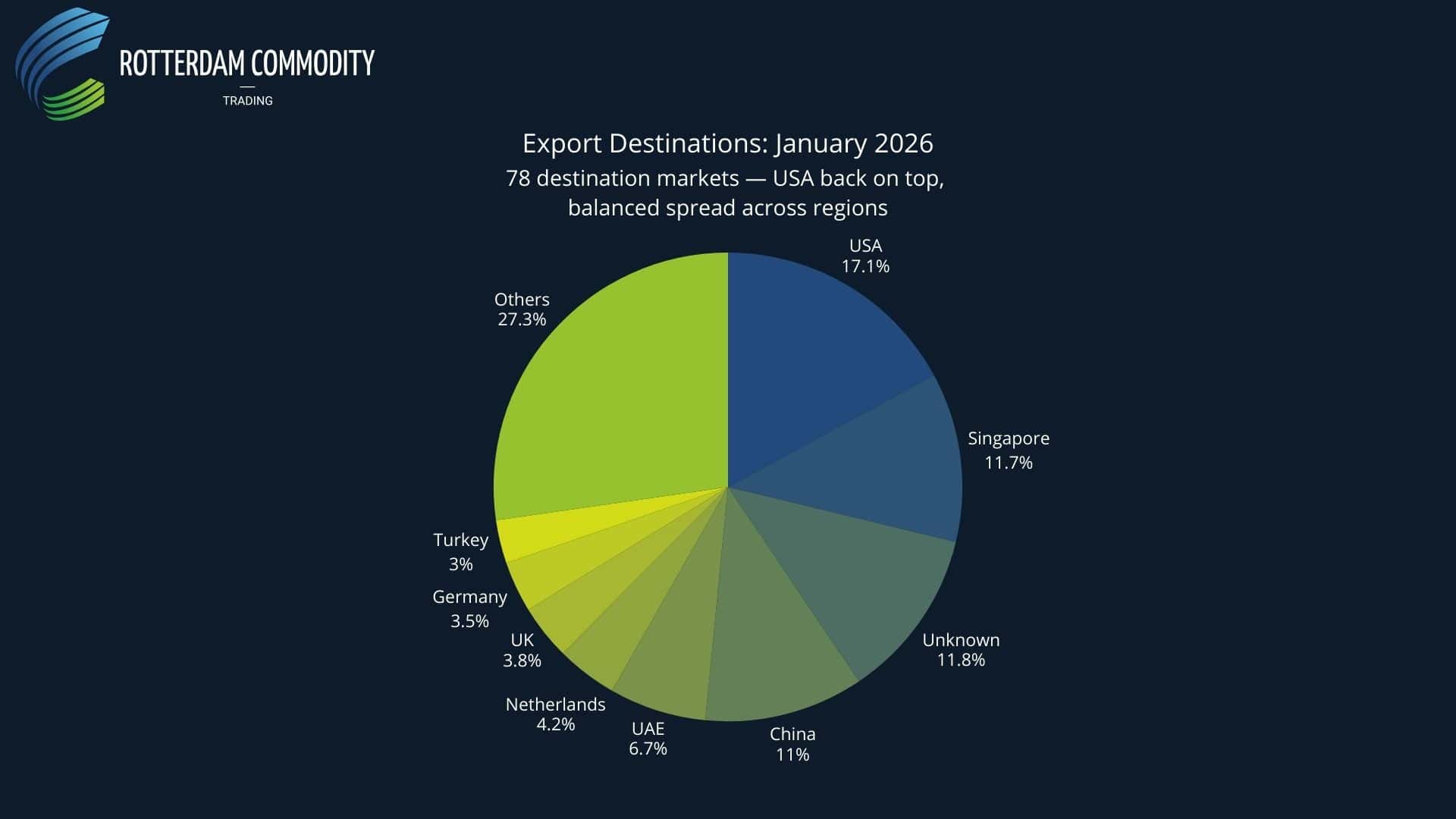

Export Destinations: The U.S. Rebounds, China Holds, Europe Dominates

The destination breakdown for January 2026 reveals a more balanced picture than the China-dominated second half of 2025.

The United States reclaimed the top position with 9,662 tons (17.1% share), representing a strong 32.4% year-on-year increase in volume and a 35.1% increase in value. This is a notable reversal from the tariff-dampened flows of mid-2025, and suggests that U.S. buyers may be rebuilding inventory after a prolonged period of destocking.

China maintained significant volume at 6,205 tons (11.0% share), ranking fourth by destination after Singapore (6,582 t, 11.7%) and a substantial “unknown” category (6,625 t, 11.8%), the latter largely representing goods shipped to bonded warehouses without declared final destinations. China’s January surge of +162.7% YoY reflects Lunar New Year-driven procurement.

The EU and other markets collectively absorbed 40,507 tons (roughly 71.9% of total exports) up 35.1% YoY. Within Europe, the Netherlands (2,347 t), the UK (2,129 t), and Germany (1,950 t) led the way. The UAE continued its expansion as a re-export hub, taking 3,793 tons.

A remarkable 321 Vietnamese companies participated in kernel exports in January, a highly fragmented exporter base. Olam’s Bien Hoa facility alone accounted for nearly USD 42.6 million (11% of total value). Other leading exporters include Long Son JSC and Long Son Inter Foods, Cao Phat, Dai Loc Phat, Thien Ky BP, and Hoang Son 1. VINACAS members collectively represented about 49.6% of total export value, meaning more than half of Vietnam’s cashew exports now come from non-member companies.

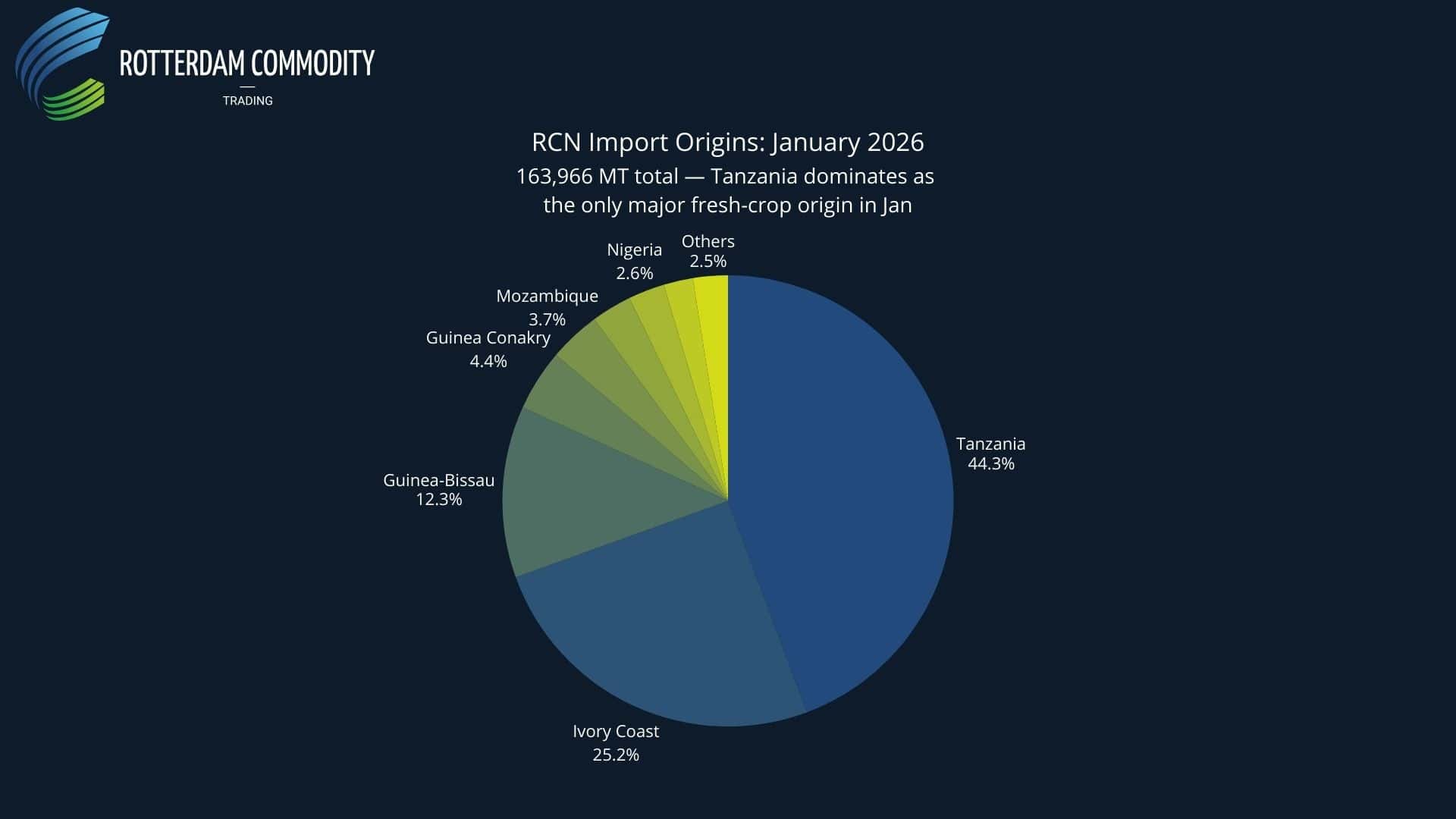

Raw Nut Imports: Tanzania Dominates the Off-Season

January’s RCN import data tells the most dramatic story of the month. Vietnam imported 163,966 tons of raw cashew nuts, up 36.1% year-on-year. Total import value reached USD 252.7 million (+20.1%). But the average import price fell to USD 1,541 per ton, down 11.7% from January 2025.

This is a significant shift from the dynamic that defined 2025, when both volume and price were climbing simultaneously. In January 2026, processors are securing more raw material at lower unit cost. Whether this reflects genuine easing in origin prices or simply a different geographic mix is the key question.

The answer lies largely in the sourcing breakdown, which must be understood in seasonal context. In January, only a handful of origins have fresh crop available, primarily Tanzania, alongside smaller volumes from Indonesia and Brazil. The West African season (Ivory Coast, Guinea-Bissau, Nigeria, Ghana) has not yet opened, and Cambodia’s harvest does not begin until February or March. This means Tanzania’s dominance of January supply is less a structural shift and more a reflection of seasonal timing:

Tanzania topped the rankings with 72,645 tons (44.3% share), comfortably the largest single origin. Tanzanian RCN has found a natural window here: with minimal competition from other fresh-crop origins, Vietnamese processors have been absorbing Tanzanian production at scale.

Ivory Coast shipped 41,256 tons (25.2% share), ranking second. The year-on-year comparison is extreme: volume is up 626.7% and value up 604.8% compared to January 2025. However, this says more about last January than this one, January 2025 saw near-total collapse of Ivorian shipments to Vietnam amid tight export conditions. This year’s January volumes likely represent carryover stock from the previous campaign, as the new Ivorian marketing season was only set to open in early February 2026, with a minimum farmgate price of 400 CFA/kg, down 6% from last year’s 425 CFA/kg.

Cambodia shipped just 771 tons in January 2026, down 81.3% from approximately 4,130 tons in January 2025. This is entirely seasonal, the Cambodian harvest typically starts in February or March, so both Januarys are off-season. The difference is one of degree, not of trend. Cambodia supplied roughly 1 million tons across full-year 2025 and will remain Vietnam’s structural anchor once the new season begins in the coming weeks. The real question is not whether Cambodia shows up, but whether the 2026 harvest matches the exceptional volumes of 2025.

Other notable origins include Guinea-Bissau (20,153 t, 12.3%), Guinea Conakry (7,146 t), Mozambique (6,031 t), Indonesia (4,832 t), Nigeria (4,309 t), and Ghana (3,412 t). In total, 15 countries supplied RCN to Vietnam in January.

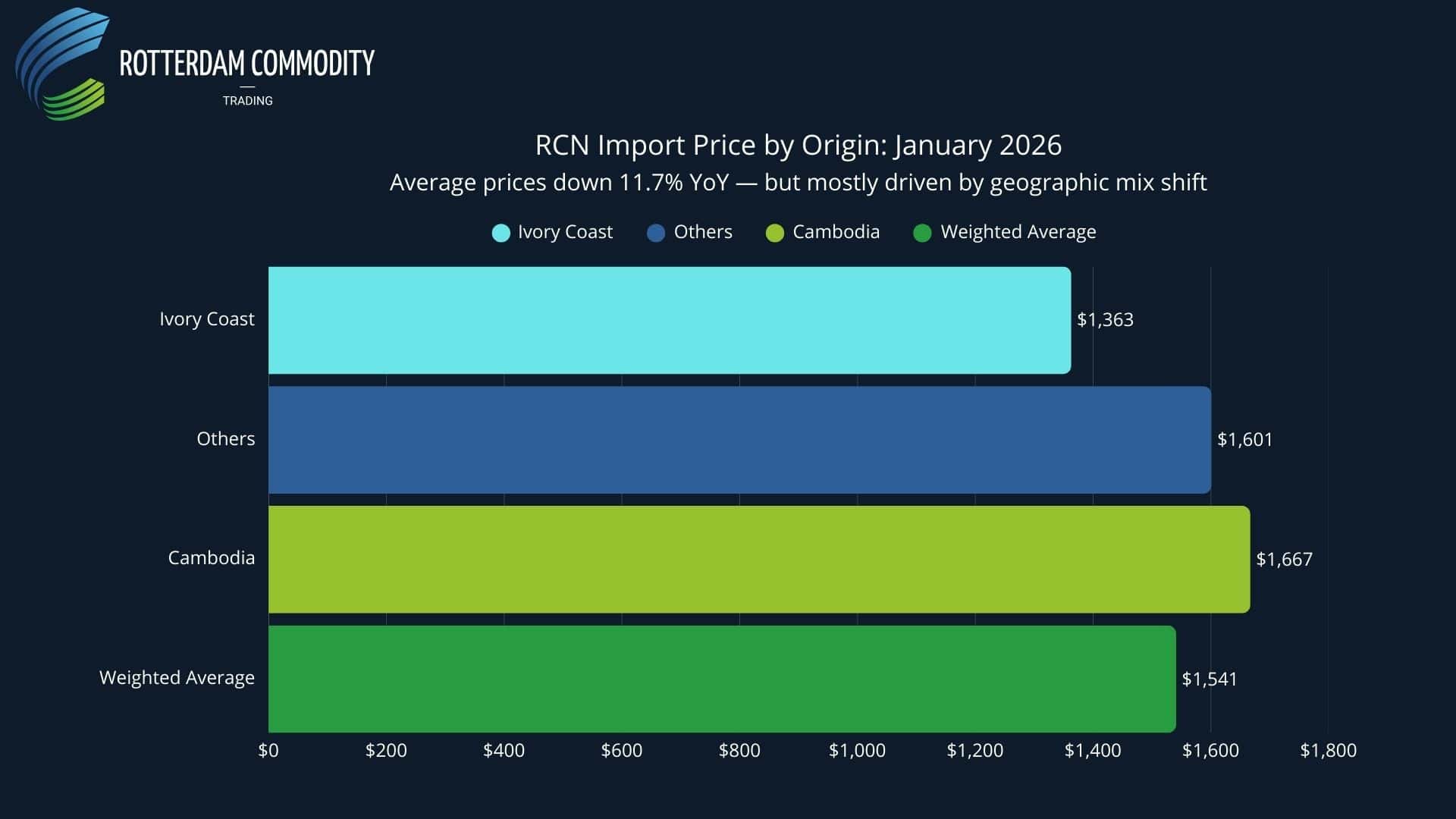

Import Prices: Cheaper on Average, but Geography Explains Most of It

The price picture across origins is uneven. Ivory Coast RCN averaged USD 1,363/ton in January, down just 3.0% YoY, making it the cheapest major origin. Cambodian RCN, in its limited volumes, averaged USD 1,667/ton, the most expensive origin, though only marginally lower (-1.2%) than a year ago. Other markets averaged USD 1,601/ton, down 9.3% YoY.

The overall weighted average of USD 1,541/ton is down 11.7% from last January. But this decline is largely compositional: the shift toward Tanzanian and other African origins, which tend to trade at lower premiums than Cambodian material, explains most of the headline price drop. This is not necessarily good news for processors. Cheaper African RCN often comes with higher moisture, lower outturn ratios, and greater quality variability compared to Cambodian supply, meaning the effective cost per kilogram of usable kernel may not have fallen as much as the import price suggests.

Borma and Kernel Imports: Volume Doubles, but Transparency Lags

Imported cashew kernels in testa (borma cashews) and white kernels totaled 14,370 tons in January, more than double (+105.2%) the same month in 2025. Import value reached USD 90.2 million (+102.1%), at an average price of USD 6,279/ton (–1.5% YoY).

When converted into RCN equivalent, these kernel imports account for approximately 26.9% of total raw material inflow, a substantial share that underscores how integrated Vietnam’s processing chain has become with semi-processed material from origin countries.

Ivory Coast 2026: A New Season Opens Under Pressure

While January’s VINACAS data only captures shipments from Ivory Coast’s old-crop stock, the broader picture for 2026 is already taking shape. Ivory Coast’s new marketing season opened in early February 2026, with national output forecast at 1.5 to 1.7 million tons, roughly in line with the 1.54 million tons produced in 2025. The minimum farmgate price was set at 400 CFA/kg, a 6% reduction from last year’s 425 CFA/kg, reflecting weaker international prices and lingering uncertainty about global demand, particularly from the U.S.

Crucially, the Ivorian processing industry has been scaling up rapidly. By some estimates, Ivory Coast processed around 600,000 tons of cashew nuts in 2025, a dramatic increase that means a growing share of Ivorian RCN stays in-country rather than being shipped to Vietnam or India. For Vietnamese processors, this trend matters: even if Ivory Coast’s total production holds steady, the exportable surplus available for Asian buyers could continue to shrink.

What January’s Numbers Mean for the Months Ahead

January 2026 paints a picture of an industry that has entered the year at full speed. Processors are shipping at a strong pace, sourcing raw material from a wider and more African-heavy origin mix, and importing significant volumes of semi-processed kernels to feed their lines.

But several structural tensions deserve close monitoring:

The Cambodia season. Cambodia’s harvest is weeks away. Once it begins, it will determine whether Vietnam can sustain the kind of throughput that January’s numbers suggest. After an exceptional 2025 campaign of roughly 1 million tons, any shortfall in the 2026 Cambodian season would put significant pressure on the supply balance.

Ivory Coast’s exportable surplus. With IVC’s domestic processing capacity expanding and farmgate prices set lower, the key question is not just how much Ivory Coast produces, but how much of that production is available for export to Vietnam. A growing Ivorian processing sector absorbing more of the crop could structurally reduce RCN supply to Vietnam, even in a stable or growing production year.

Flat export prices amid volume growth. Kernel export prices that do not rise with volumes suggest that competitive pressure or buyer resistance is capping the upside. Processors need volume just to maintain revenue, not to grow margins.

Traceability risk in kernel imports. Over 70% of imported borma cashews arriving without declared origin is a compliance liability that will only become more difficult to sustain as destination markets increase supply chain scrutiny.

The Bottom Line

Vietnam’s cashew machine is running at high speed to start 2026. Exports are strong, sourcing is diversified across African origins, and lower average RCN prices offer some cost relief compared to the peaks of 2025.

But this is a January picture, a snapshot taken during the inter-harvest lull, when Tanzania is the only major origin with fresh crop on the market and Cambodia has yet to begin its season. The composition of supply will look entirely different by April, when Cambodian volumes arrive, Ivory Coast’s new season reaches full pace, and the other West African origins come to market.

The real story of 2026 will be written between now and June. How Cambodia’s harvest unfolds, whether Ivory Coast’s growing domestic processing leaves less RCN for Vietnam, and whether kernel prices can firm up against rising volumes, these are the questions that will define the year. For now, the machine is running. The question is whether the inputs will keep flowing at the pace the machine demands.

For weekly monitoring of Vietnam, Cambodia, West Africa, and global cashew flows, including weather risk, yield signals, and trade dynamics; subscribe to our updates.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.