Vietnam’s cashew sector did not stay in February’s recalibration mode for long. After January’s export burst and February’s pause, March brought a sharp reacceleration in both exports and imports. Kernel shipments rebounded to 57,581 metric tons, while raw cashew nut imports surged to 475,684 tons. The defining change was on the supply side: Cambodia moved from near-absence in January, to a meaningful return in February, to outright dominance in March. But the price story moved in the opposite direction. Kernel FOB indicators softened again, suggesting that Vietnam’s processors are regaining throughput faster than they are regaining pricing power.

Kernel Exports: Volume Rebounds, Pricing Still Slips

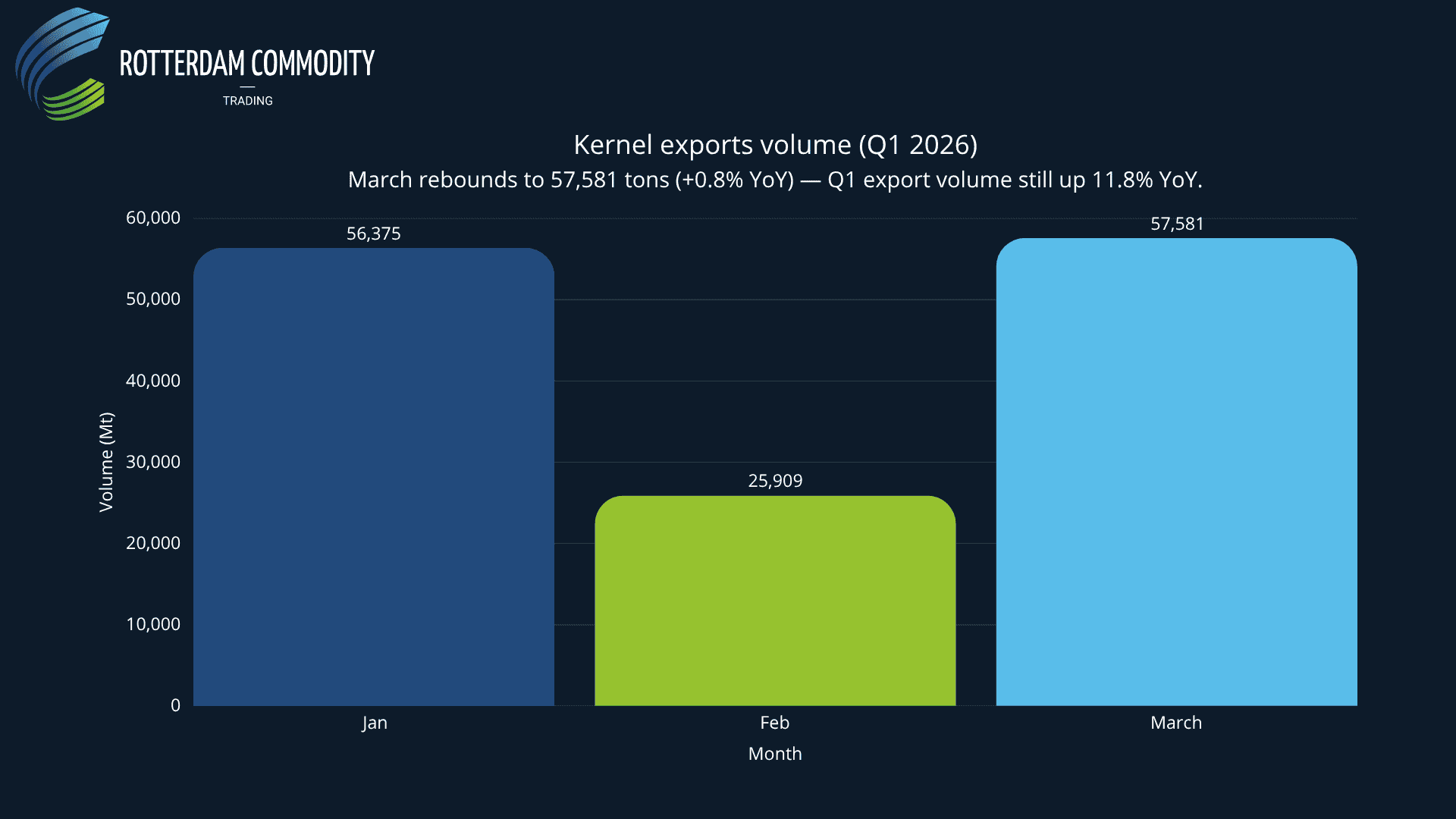

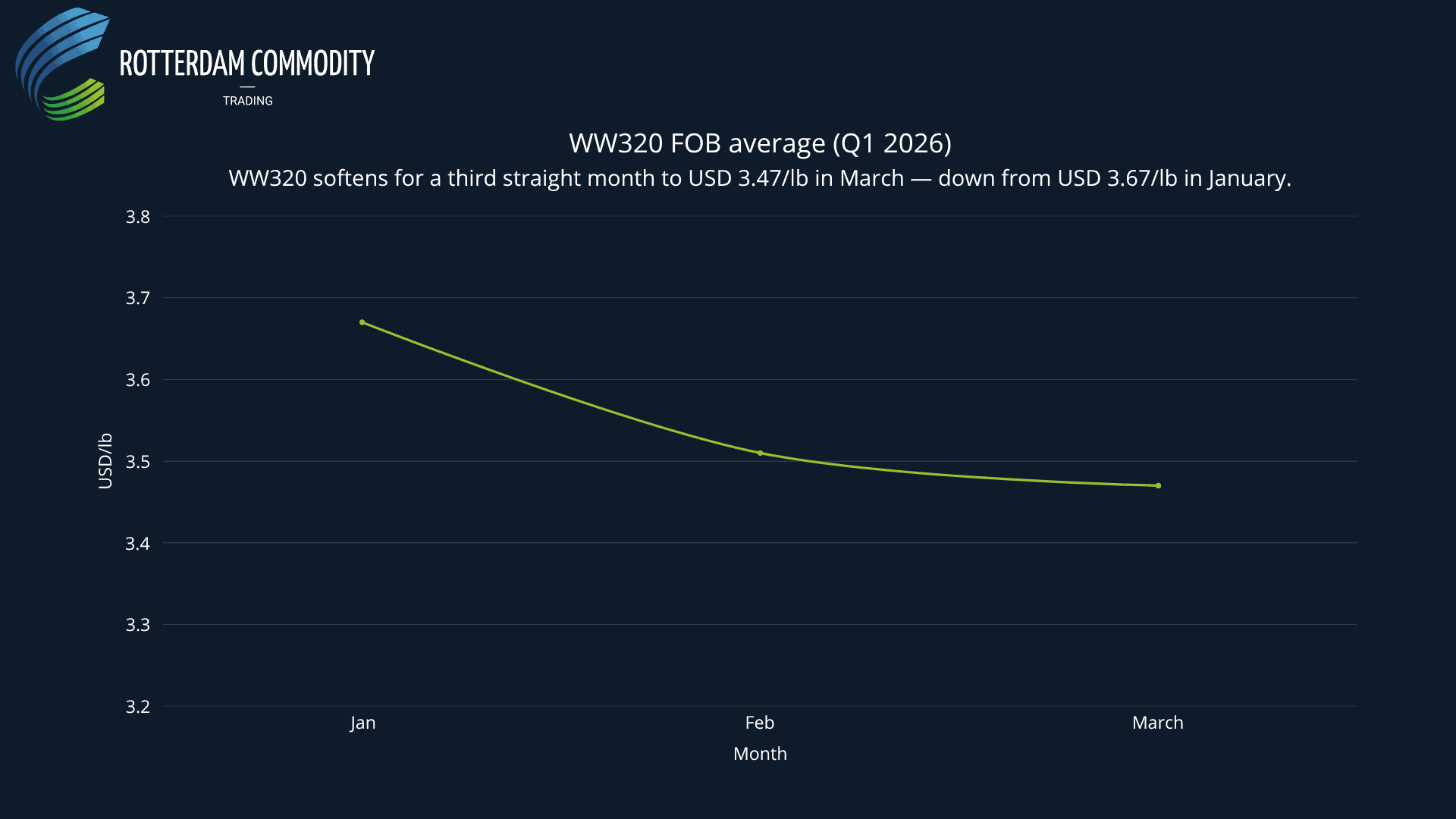

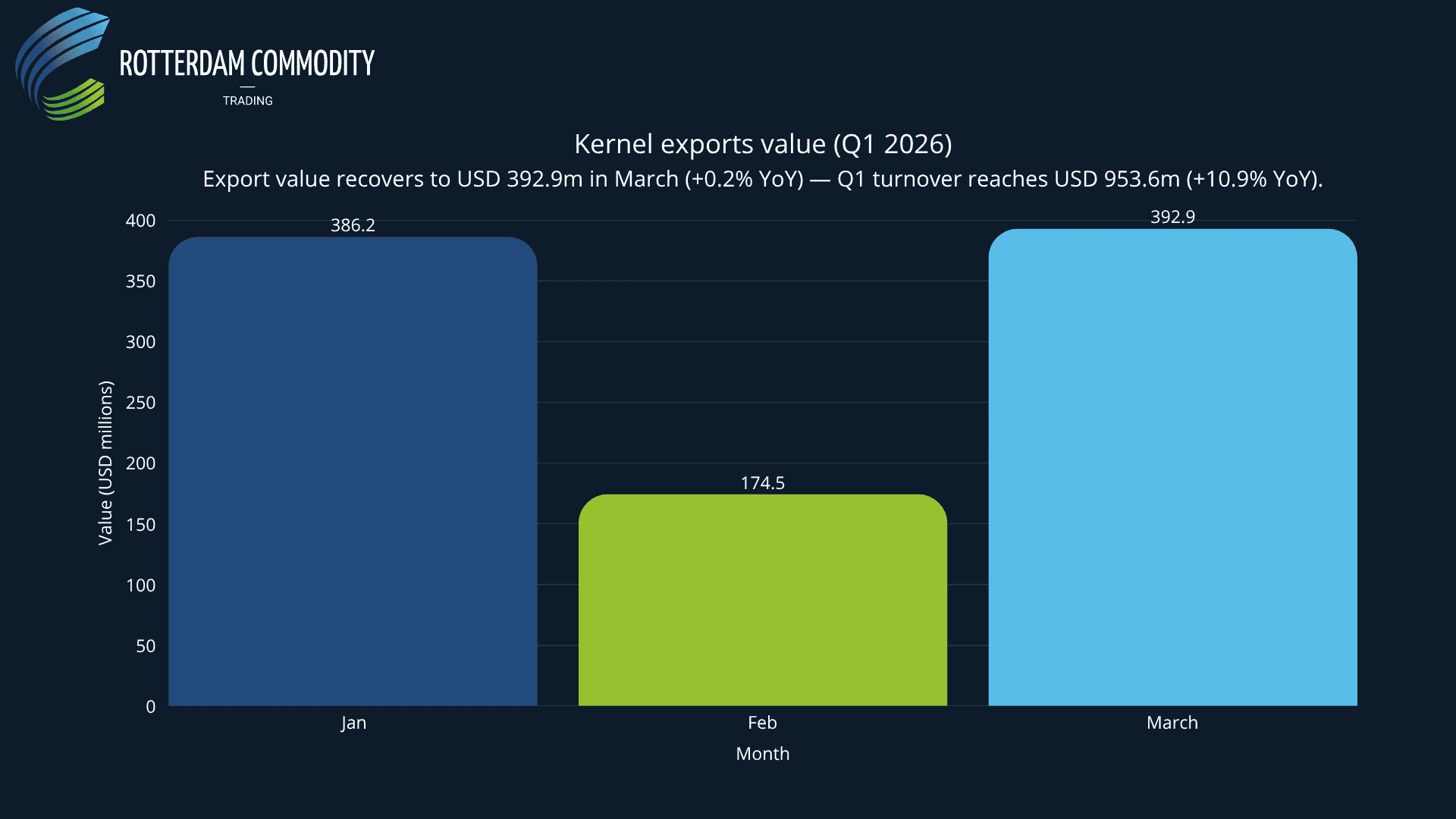

Vietnam exported 57,581 tons of semi-processed cashew kernels in March 2026, up 0.8% year-on-year, with export turnover of USD 392.9 million, up 0.2%. That marks a strong recovery from February’s 25,909 tons and brings March back close to January’s 56,375-ton level. Yet the rebound in volume did not come with firmer pricing. The average export price in March was USD 6,824 per ton, down 0.6% year-on-year. The same pattern is visible in WW320 FOB quotations: the March range was USD 3.00 to USD 3.95/lb, averaging USD 3.47/lb, down from USD 3.51/lb in February and USD 3.67/lb in January. In other words, Vietnam’s export machine regained speed in March, but the market paid less for each pound than it did at the start of the quarter.

The first-quarter picture remains clearly positive in aggregate. Across January to March, Vietnam exported 139,865 tons of kernels worth USD 953.6 million, up 11.8% in volume and 10.9% in value versus the same period in 2025. The cumulative average export price of USD 6,803/ton is only 1.1% below last year and still well above VINACAS’s annual plan price of USD 6,250/ton. By the end of March, the sector had already reached 17.5% of its annual export volume plan and 19.1% of its export value plan. That is a solid first-quarter pace, even if March shows that price support is becoming less reliable than volume support.

Export Destinations: The U.S. Stays Strong, China Recovers Only Partly

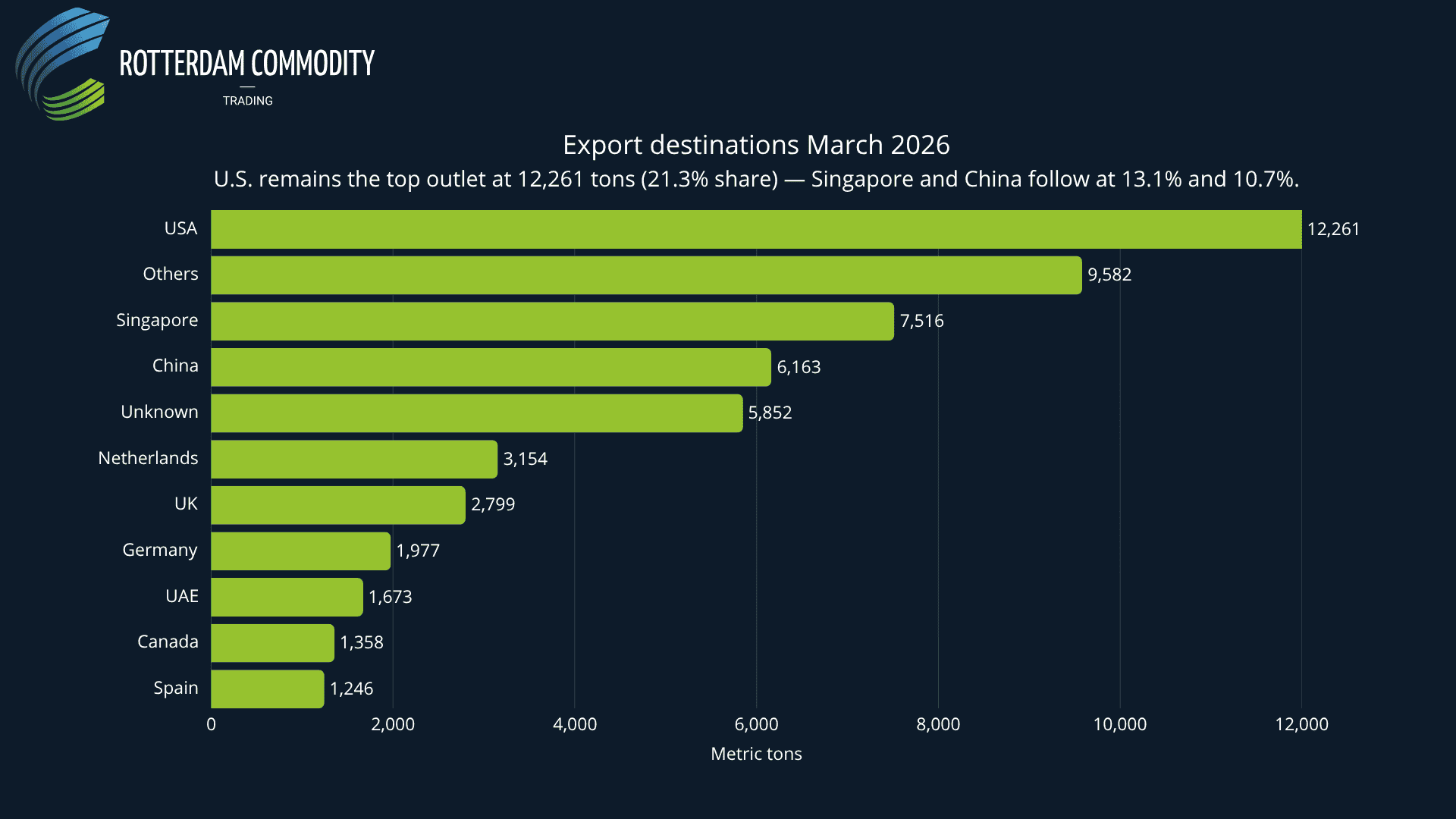

The destination mix in March reinforces a theme already visible in the earlier January and February releases: the United States remains Vietnam’s steadiest growth market in early 2026. U.S. imports reached 12,261 tons in March, equal to 21.3% of total kernel exports for the month, and up 29.4% year-on-year. Over the full first quarter, U.S. shipments totaled 26,745 tons, up 29.7% year-on-year. That consistency matters. January showed a strong U.S. return, February confirmed it was not a one-off, and March strengthened the case that American buyers have been rebuilding positions in a sustained way rather than through a single burst of purchasing.

China, by contrast, has not fully re-established the momentum seen in January. March exports to China recovered to 6,163 tons from February’s Lunar New Year-distorted 845 tons, but they were still down 31.2% year-on-year for the month. On a January-March basis, China took 13,213 tons, down 12.6% in volume and 3.3% in value from the same period last year. That leaves the market with a familiar split: strong Western demand, especially from the U.S., alongside a China flow that remains meaningful but less dependable than it looked in January’s pre-holiday surge. The broader EU-and-other-markets category absorbed 39,158 tons in March, up 1.2% year-on-year, bringing the first-quarter total to 99,907 tons, up 11.7%. Singapore was the second-largest single March destination at 7,516 tons, ahead of China.

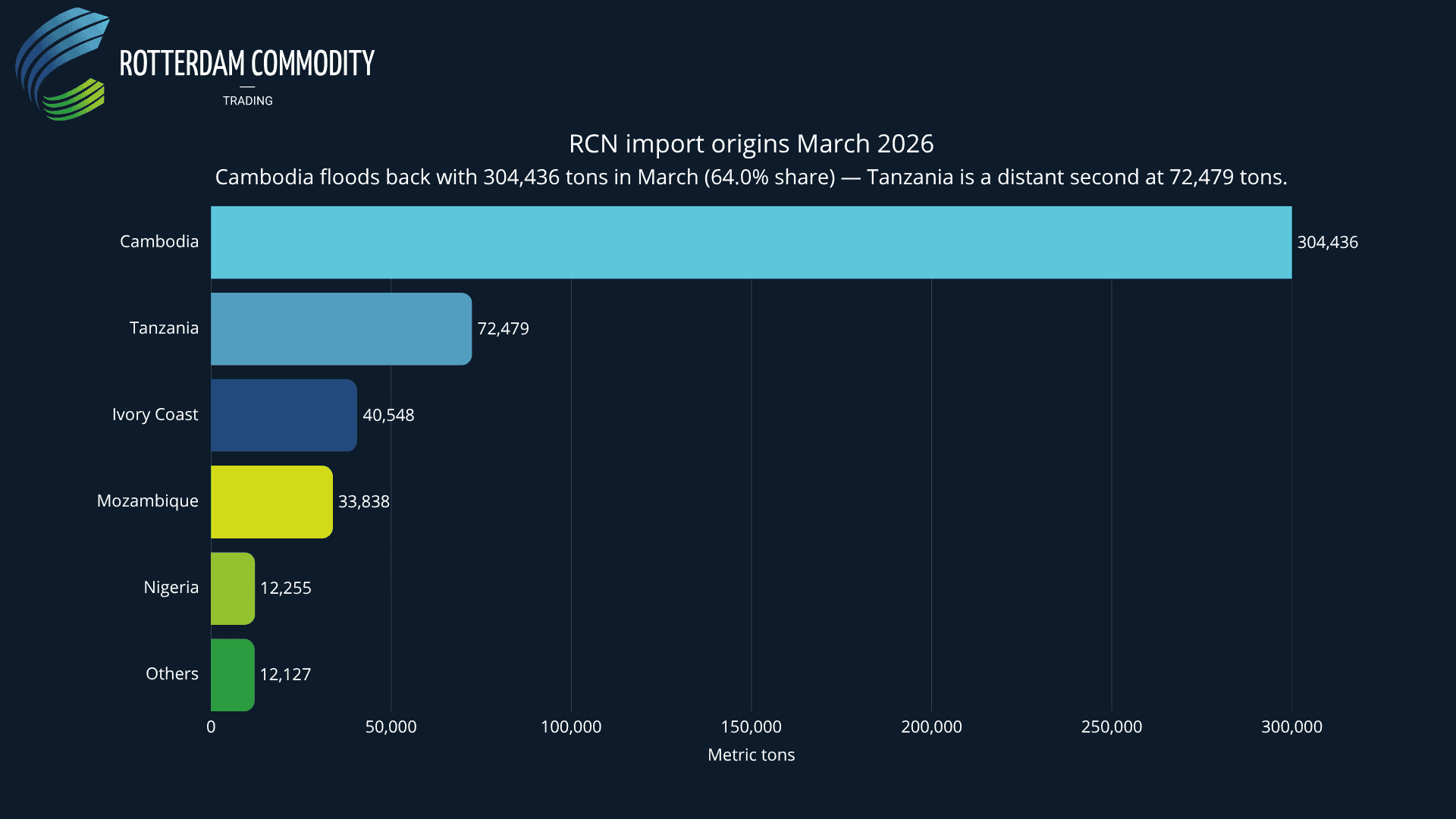

Raw Nut Imports: Cambodia Moves From Return to Dominance

If February’s key story was that Cambodia had returned, March’s story is that Cambodia took over. Vietnam imported 475,684 tons of raw cashew nuts in March, up 44.6% year-on-year, with import value rising 57.1% to USD 794.1 million. Cambodia alone supplied 304,436 tons, equal to 64.0% of March’s total import volume. Tanzania followed far behind at 72,479 tons, or 15.2%, while Ivory Coast supplied 40,548 tons and Mozambique 33,838 tons. Nigeria added 12,255 tons. This is the clearest sign yet that the Cambodian 2026 season is now fully driving Vietnam’s processing pipeline. January was defined by Tanzania’s seasonal window and Cambodia’s absence; February marked Cambodia’s return with 56,240 tons; March turned that return into dominance.

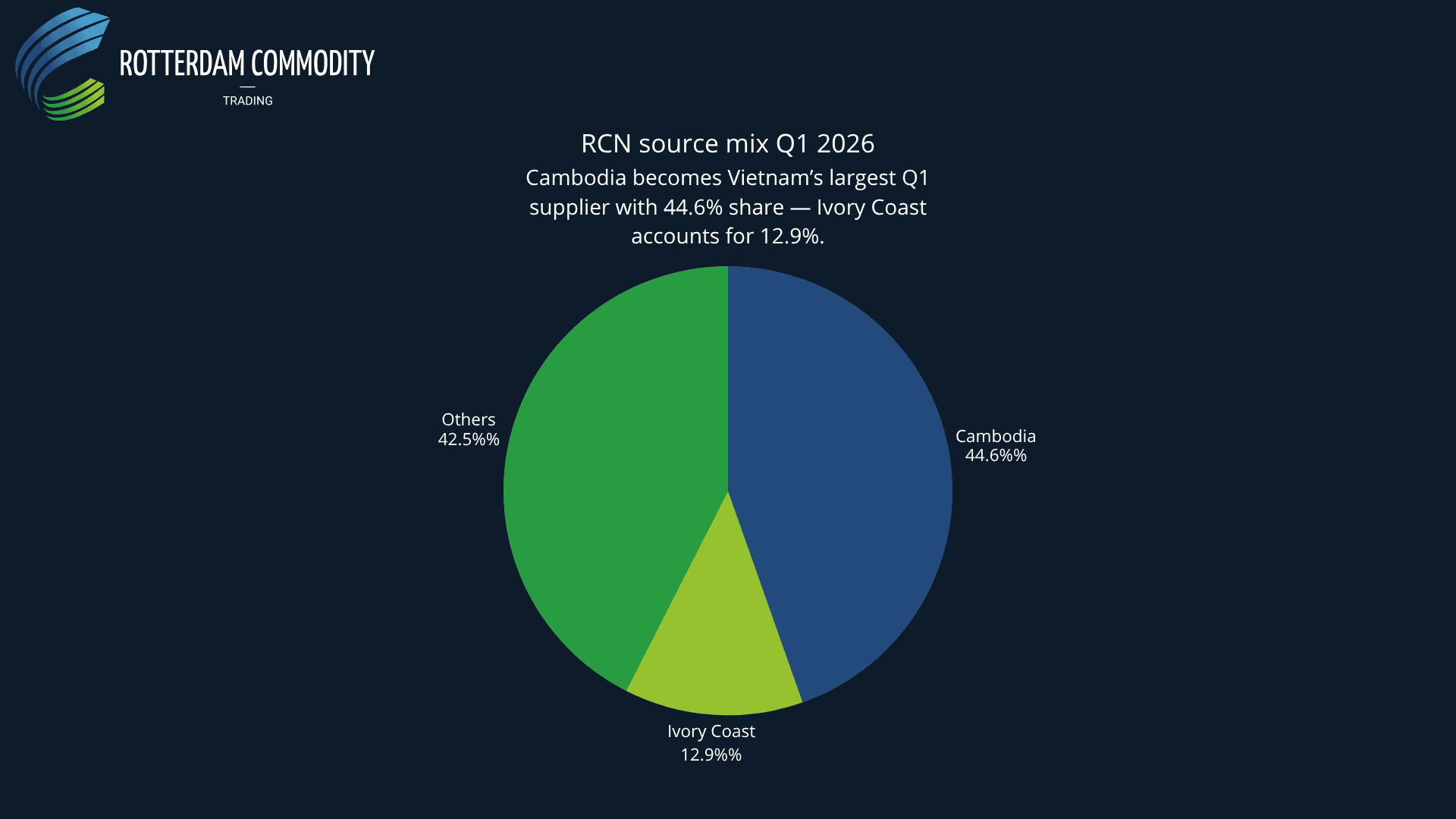

The cumulative first-quarter import picture is striking. Vietnam brought in 810,084 tons of raw cashew nuts worth USD 1.314 billion in the first three months of 2026, up 35.9% in volume and 36.3% in value year-on-year. Cambodia accounted for 361,446 tons over the quarter, making up 44.6% of all Q1 raw nut imports, ahead of the grouped “other markets” at 42.5% and Ivory Coast at 12.9%. By the end of March, Vietnam had already reached 25.3% of its annual raw nut import volume plan and 31.6% of its annual import value plan. Supply availability, at least in headline tonnage terms, is not the problem. The more important question is what this origin mix means for cost, yield efficiency, and eventual kernel margins.

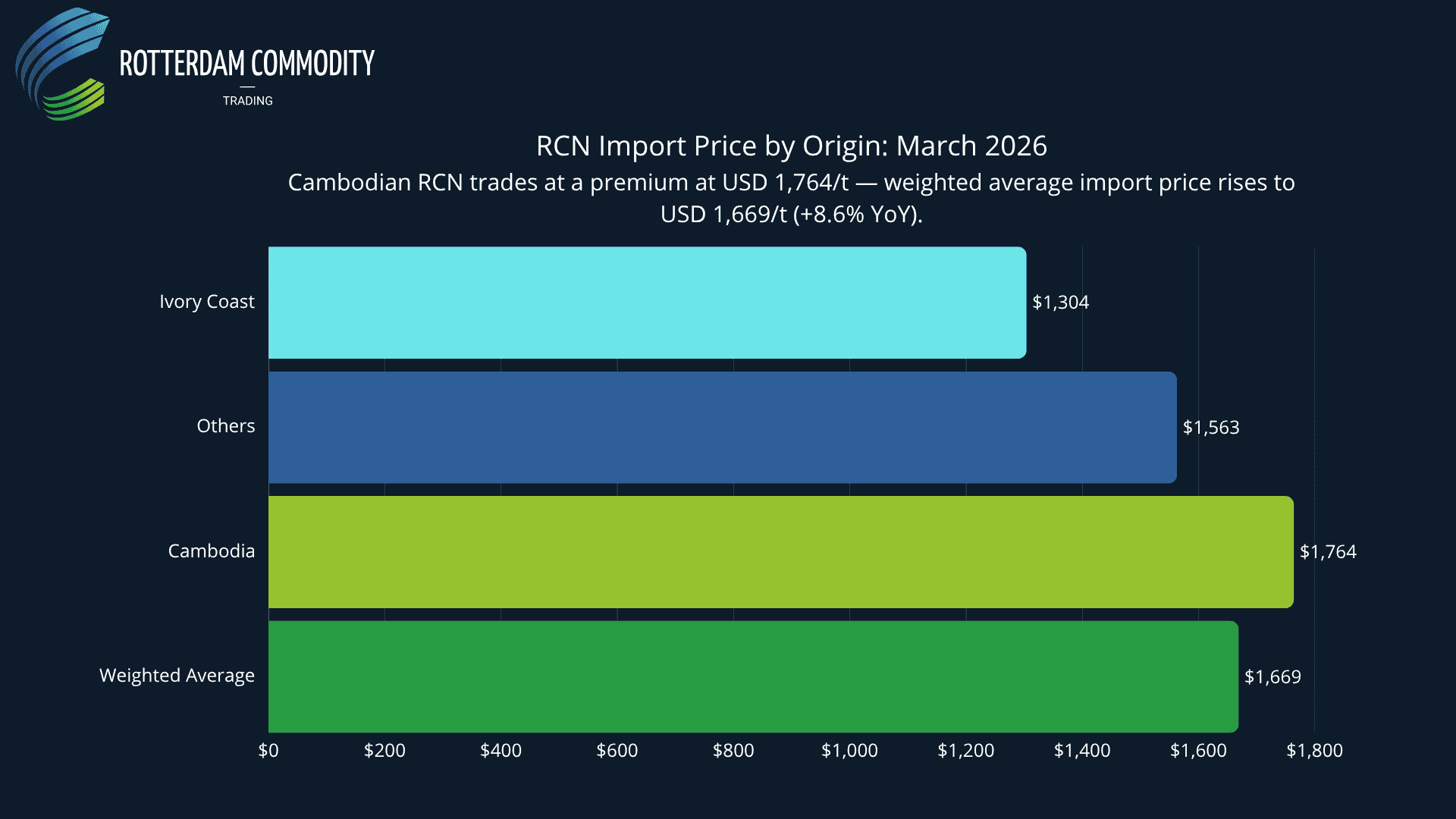

Import Prices: The Mix Shift Has Reversed

March also changed the import price picture. In January and February, the African-heavy sourcing mix helped keep the average raw nut import price relatively subdued, at USD 1,541/ton and USD 1,570/ton respectively. In March, the average jumped to USD 1,669/ton, up 8.6% year-on-year. That move reflects geography more than scarcity. Cambodian raw nuts averaged USD 1,764/ton in March, well above Ivory Coast at USD 1,304/ton and above the “other markets” average of USD 1,563/ton. When Cambodia takes 64% of the monthly import mix, the headline price rises with it.

That creates a more complicated margin setup than the headline import volume suggests. Cambodia is Vietnam’s preferred structural supplier for a reason, but it is not the cheapest one. VINACAS also reiterates the processing-efficiency issue: Cambodian cargoes with 10–15% moisture require around 5.0–5.3 kg of raw nuts per 1 kg of exported kernel, while fresh, higher-moisture lots at 16–30% can require 6.5 kg/kg. So March brought Vietnam more Cambodian supply and more preferred origin exposure, but not necessarily cheaper effective input cost. On a cumulative January-March basis, the average raw nut import price was still only USD 1,594/ton, down 3.9% year-on-year, but that Q1 average now masks two distinct phases: an African-discounted January-February, followed by a Cambodian-premium March.

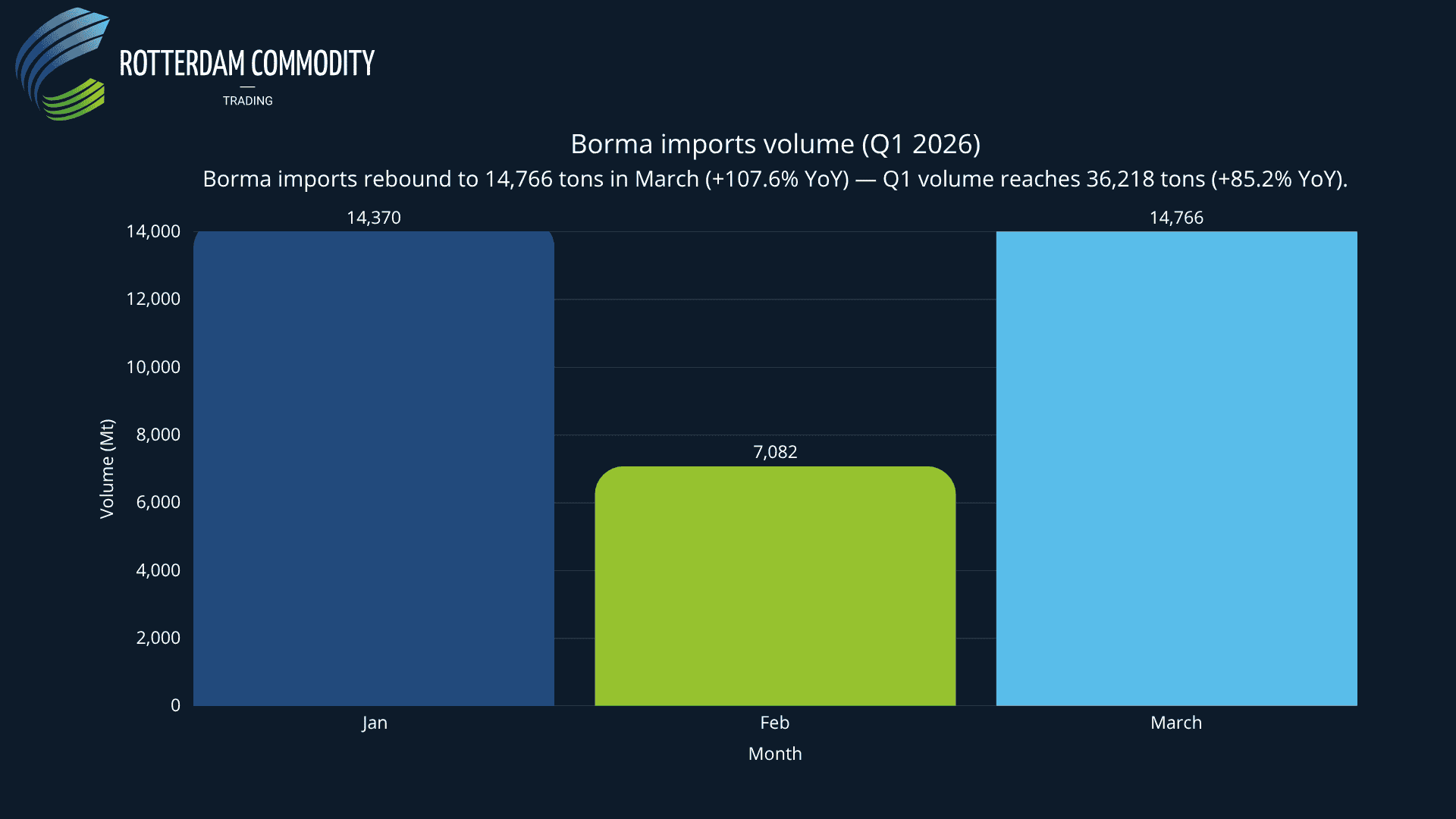

Borma Imports: Still a Structural Part of the System

March also showed that imported semi-processed material remains deeply embedded in Vietnam’s processing chain. Imported borma cashews and white kernels totaled 14,766 tons in March, up 107.6% year-on-year, with value up 87.9% to USD 92.7 million. That is effectively a return to January’s elevated level after February’s dip to 7,082 tons. Across Q1, borma imports reached 36,218 tons, up 85.2% year-on-year, at an average price of USD 6,193/ton, down 5.6%. On an RCN-equivalent basis, imported kernels represented 15.8% of Vietnam’s total raw material inflow in the first quarter. That is a meaningful share, and it suggests that even with Cambodia now flooding the pipeline, imported semi-processed cashews are not just a temporary gap-filling tool but a structural part of the operating model.

What March Means for Q2

March changes the tone of the 2026 story again. January showed that Vietnam could keep the system running at speed even without Cambodia. February showed Cambodia returning and China stepping back after Lunar New Year. March shows the next phase: Cambodia is no longer merely back, it is now the dominant supplier, while export volumes have recovered but FOB pricing continues to soften. That combination matters. Abundant raw material is positive for throughput, but lower WW320 prices and a higher-cost Cambodian import mix are not obviously positive for processing margins.

The market now has three immediate variables to watch. First, whether Cambodia can sustain anything close to March’s 304,436-ton pace into April. Second, whether the U.S. can continue absorbing large kernel volumes while China remains softer on a year-on-year basis. Third, whether Vietnam’s kernel FOB prices can stabilize after three consecutive monthly steps lower in WW320 averages from January to March. For now, the Q1 message is clear: Vietnam’s cashew sector is still running ahead of last year in both imports and exports, but the balance of advantage is shifting from price to volume. In March, supply came back faster than pricing power did.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.