Vietnam’s cashew sector moved into April with even more volume, but not with a simpler margin story. After January’s export surge, February’s recalibration and March’s reacceleration, April confirmed that the sector is now running at full speed again.

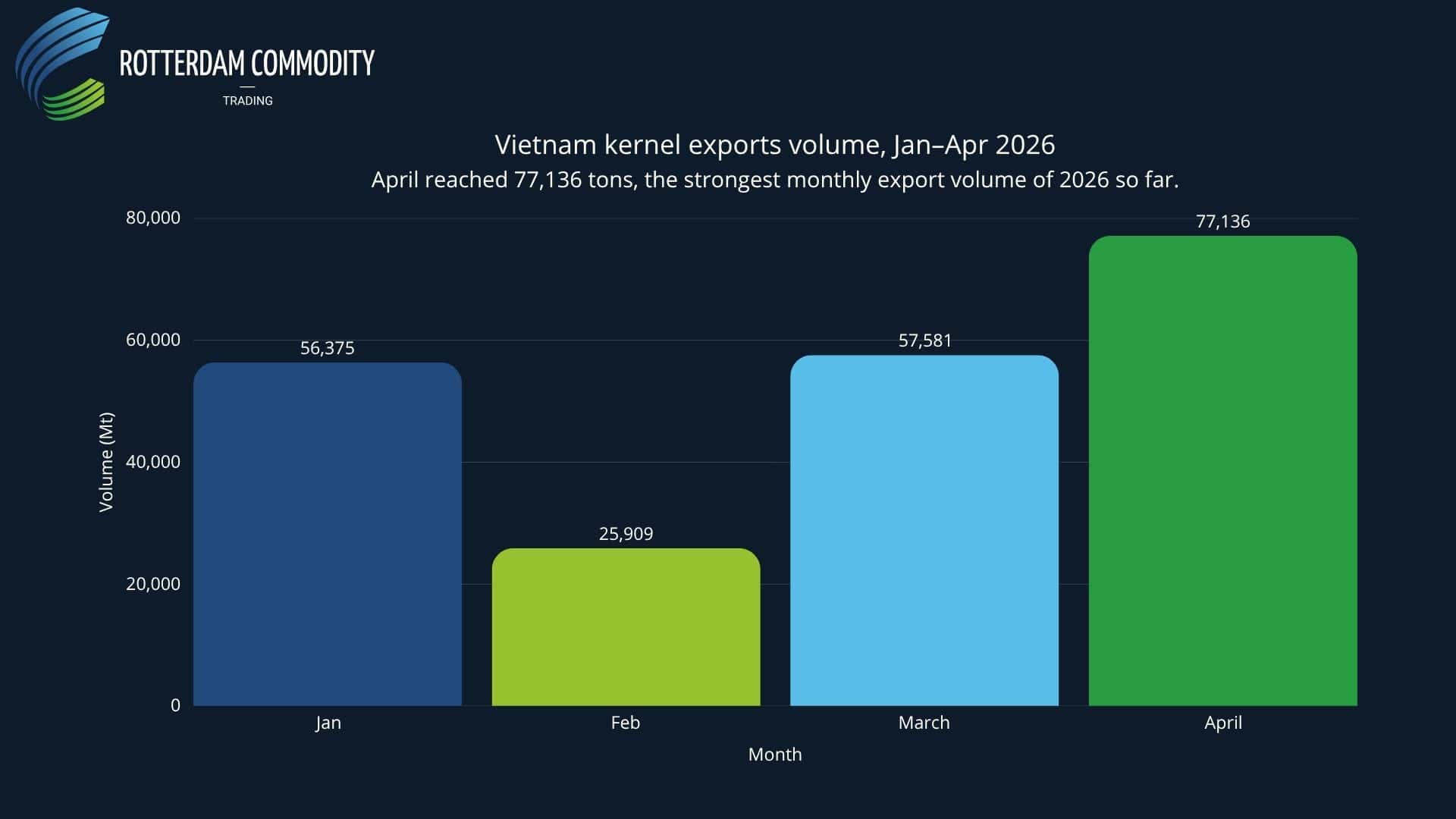

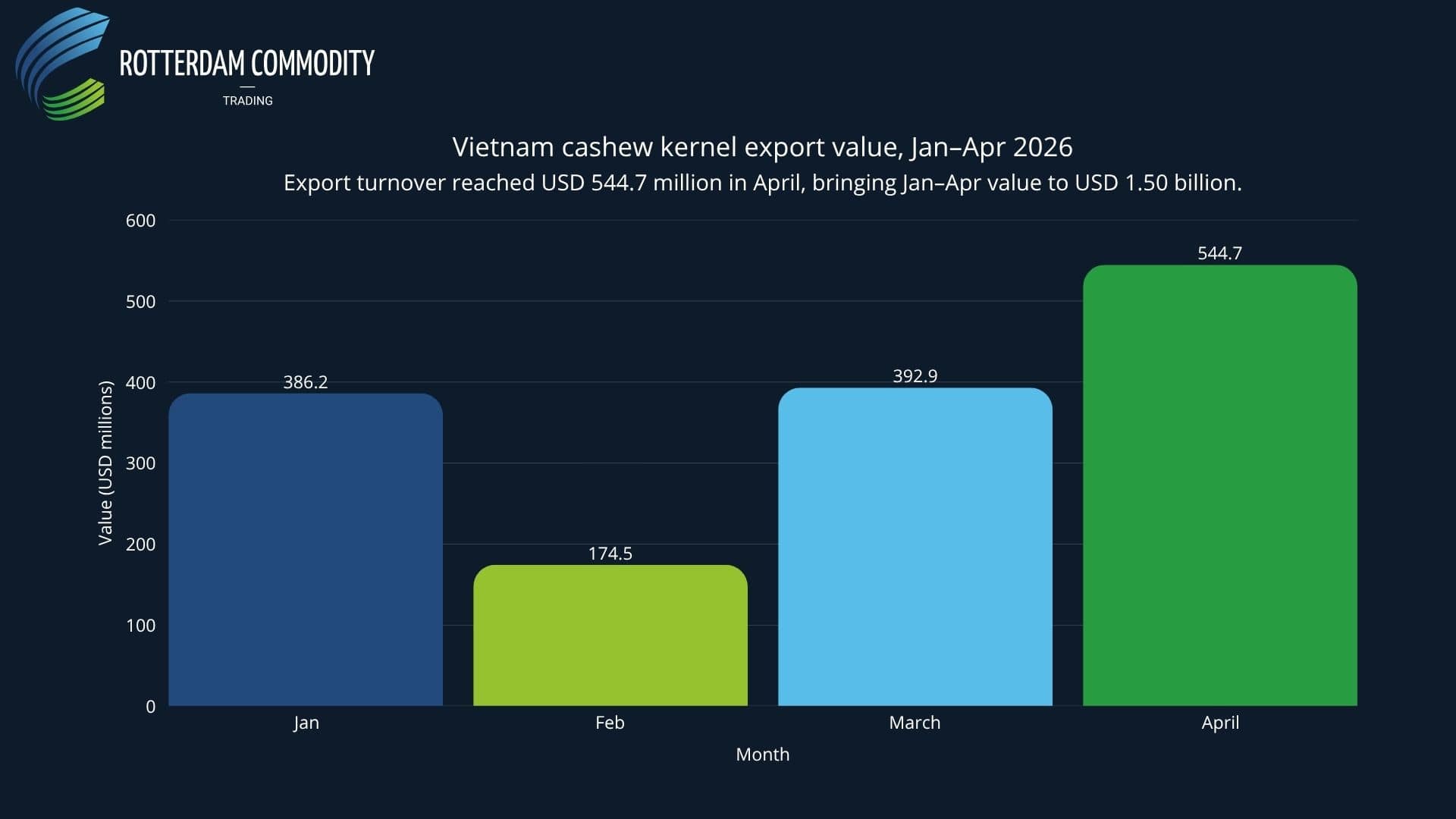

The latest VINACAS figures show Vietnam exported 77,136 metric tons of semi-processed cashew kernels in April 2026, the strongest monthly volume of the year so far. Export value reached USD 544.7 million, while the average export price rose to USD 7,061 per ton. On the supply side, raw cashew nut imports climbed further to 543,688 tons, worth USD 918.6 million.

At first glance, this is a positive picture: more kernels out, more raw nuts in, and both export and import flows comfortably ahead of last year on a cumulative basis. But the detail matters. Cambodia now dominates Vietnam’s raw nut pipeline to an exceptional degree, WW320 FOB indicators softened again, and the sector is increasingly relying on throughput rather than clear pricing power.

Kernel Exports: April Becomes the Strongest Month of 2026

Vietnam exported 77,136 tons of semi-processed cashew kernels in April, up 3.2% year-on-year. Export turnover increased more strongly, rising 8.3% to USD 544.7 million. The average export price reached USD 7,061 per ton, up 4.9% year-on-year and clearly above the levels seen in January, February and March.

This marks a sharp month-on-month acceleration. March had already represented a rebound, with exports of 57,581 tons after February’s slowdown. April went further, adding almost 20,000 tons compared with March. In other words, Vietnam’s export machine did not merely recover from the February pause; it moved into an even higher operating gear.

The cumulative picture is also solid. Across January to April, Vietnam exported 217,001 tons of kernels worth USD 1.498 billion. That is up 8.6% in volume and 9.9% in value versus the same period in 2025. The average export price for the first four months was USD 6,867 per ton, slightly above last year and nearly 10% above VINACAS’s full-year plan price of USD 6,250 per ton.

By the end of April, Vietnam had already reached 27.1% of its annual export volume plan and 30.0% of its annual export value plan. That is a healthy pace for the first third of the year. The question is no longer whether Vietnam has enough throughput. The question is whether this throughput can translate into better processor margins.

WW320: FOB Still Softens Despite Higher Export Prices

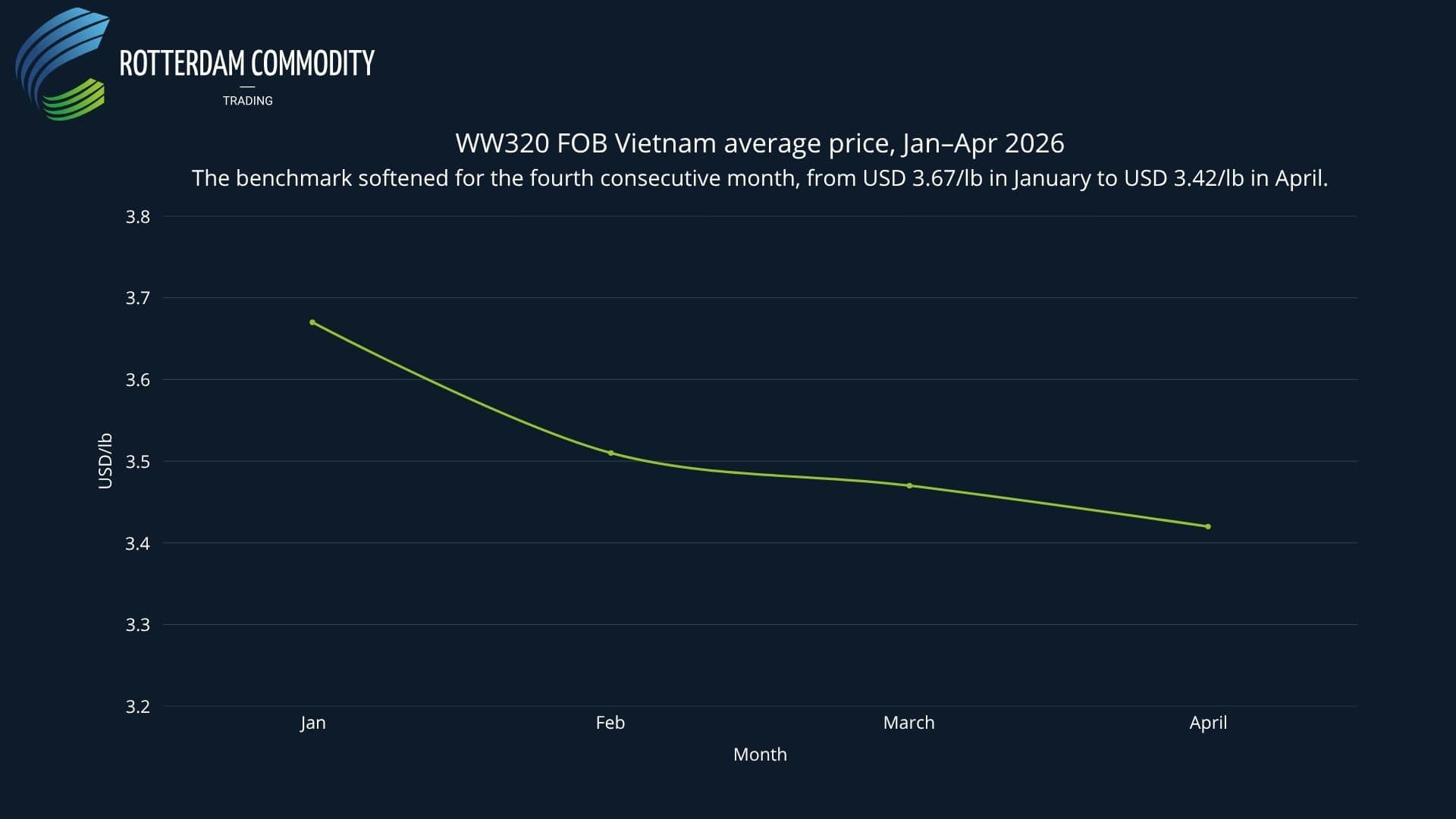

The broader export price moved higher in April, but the WW320 indicator tells a more cautious story. VINACAS reported April WW320 FOB Vietnam between USD 2.93 and USD 3.90/lb, with an average of USD 3.42/lb. That is down from USD 3.47/lb in March, USD 3.51/lb in February and USD 3.67/lb in January.

This means the benchmark has now softened for four consecutive months. The average April WW320 price was also 1.9% below the same period last year and remained around 10% below the comparable India 2025 level.

That distinction matters. The overall export price per ton improved in April, helped by destination mix and product mix, but the key FOB benchmark still points to pressure in standard kernel pricing. This supports the same theme seen in March: Vietnam is moving more product, but pricing power remains less convincing than volume growth.

Export Destinations: China Returns to First Place

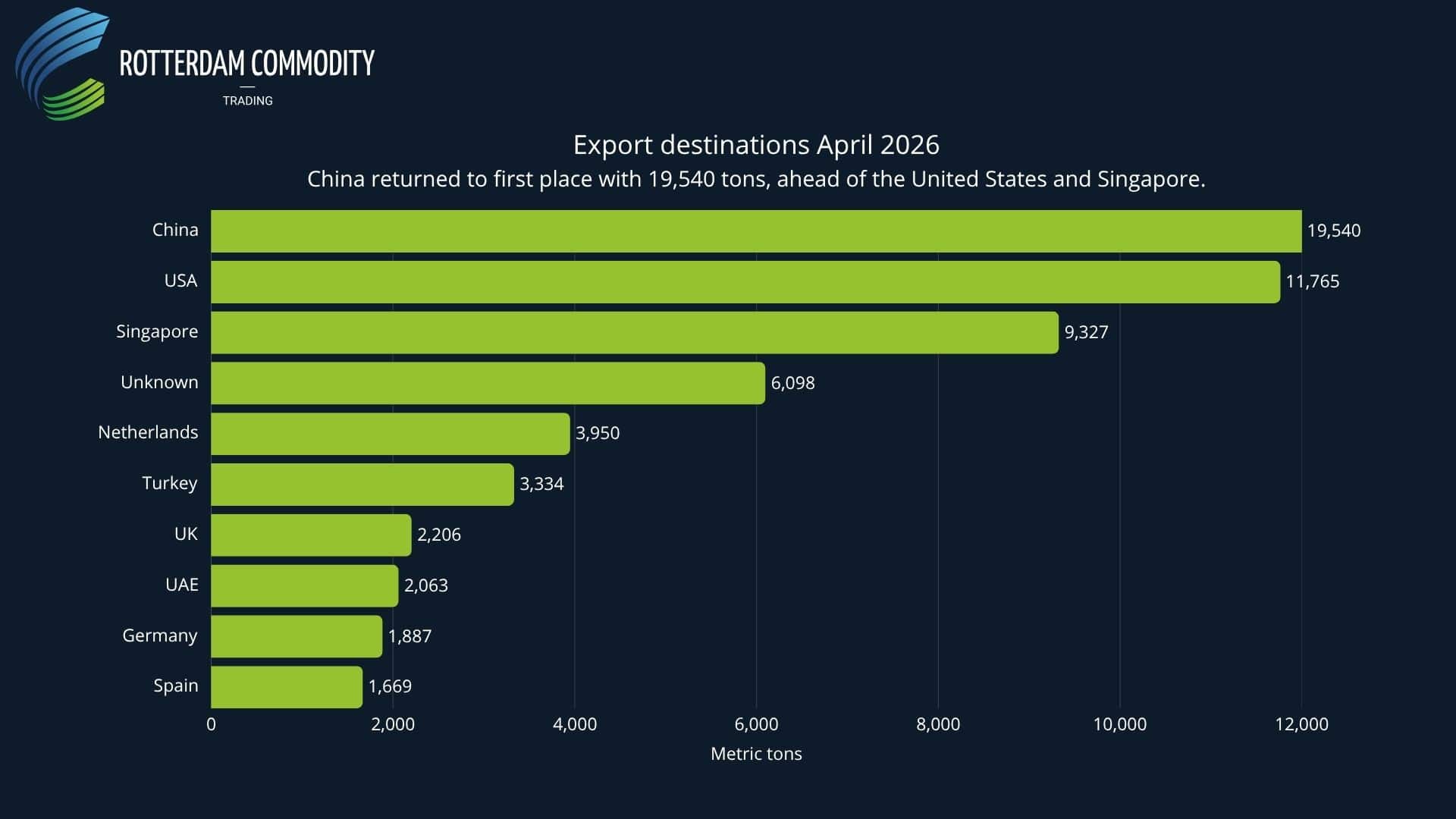

April changed the demand map. China returned as Vietnam’s largest single export destination, taking 19,540 tons of kernels worth USD 141.7 million. That represented 25.3% of Vietnam’s total kernel export volume for the month. The U.S. ranked second with 11,765 tons, followed by Singapore at 9,327 tons.

China’s April volume was still 2.7% below April 2025, but the value of shipments rose 13.0%. This reflects a much higher average price: exports to China averaged USD 7,250 per ton in April, up 16.1% year-on-year. After February’s Lunar New Year-related drop and March’s partial recovery, China is clearly back as a major buyer, but not yet in a straightforward volume-growth pattern.

The United States remains the more consistent growth story. April shipments to the U.S. reached 11,765 tons, up 31.4% year-on-year, with value rising 36.4%. Across January to April, U.S. shipments totaled 38,510 tons, up 30.2% year-on-year, with export value up 32.1%. That continues the trend already visible in the January, February and March data: U.S. demand has been steady, broad-based and far less seasonal than China’s.

The EU and other markets absorbed 45,832 tons in April, almost flat year-on-year in volume but up 1.3% in value. On a cumulative basis, this broad category remains the largest block by far, with 145,739 tons exported during the first four months, equal to roughly two-thirds of Vietnam’s total kernel shipments.

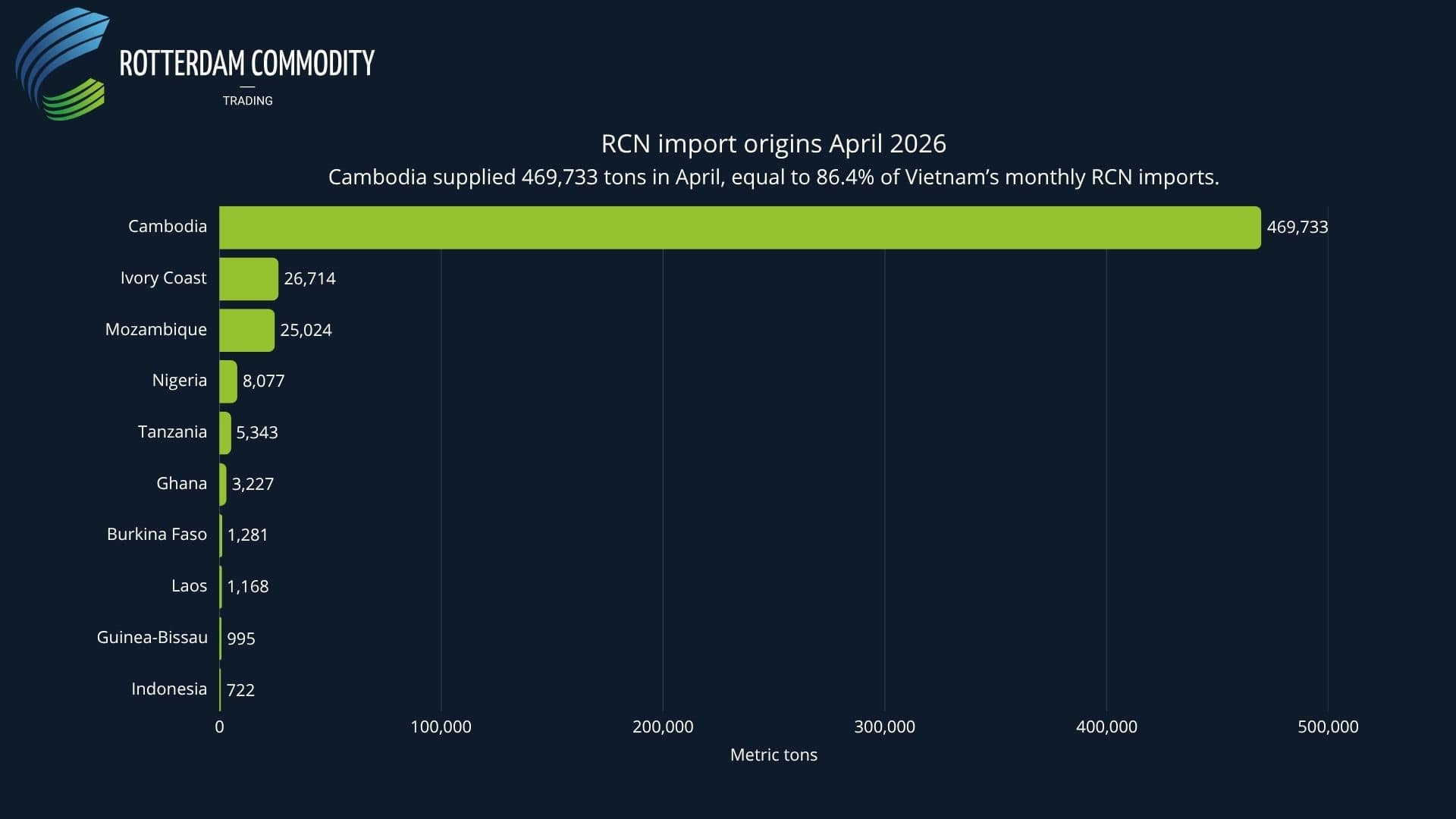

Raw Nut Imports: Cambodia Takes Over Completely

The April import picture is dominated by one number: Cambodia supplied 469,733 tons of raw cashew nuts to Vietnam in April alone. That was 86.4% of Vietnam’s total RCN import volume for the month.

This is a major escalation from March, when Cambodia had already supplied 304,436 tons and accounted for about 64% of monthly RCN imports. In February, Cambodia supplied 56,240 tons. In January, it was almost absent at just 771 tons. The season has therefore moved through four clear stages: Cambodia absent in January, returning in February, dominant in March, and overwhelmingly dominant in April.

Total RCN imports reached 543,688 tons in April, up 12.0% year-on-year, with import value rising 25.2% to USD 918.6 million. Across January to April, Vietnam imported 1.354 million tons of RCN, up 25.2% year-on-year, with import value up 31.5% to USD 2.233 billion.

By the end of April, Vietnam had already reached 42.3% of its annual RCN import volume plan and 53.7% of its annual import value plan. That confirms the strength of physical supply into Vietnam. But it also confirms that the cost side is running ahead of volume: the sector is already more than halfway through its planned import value after only four months.

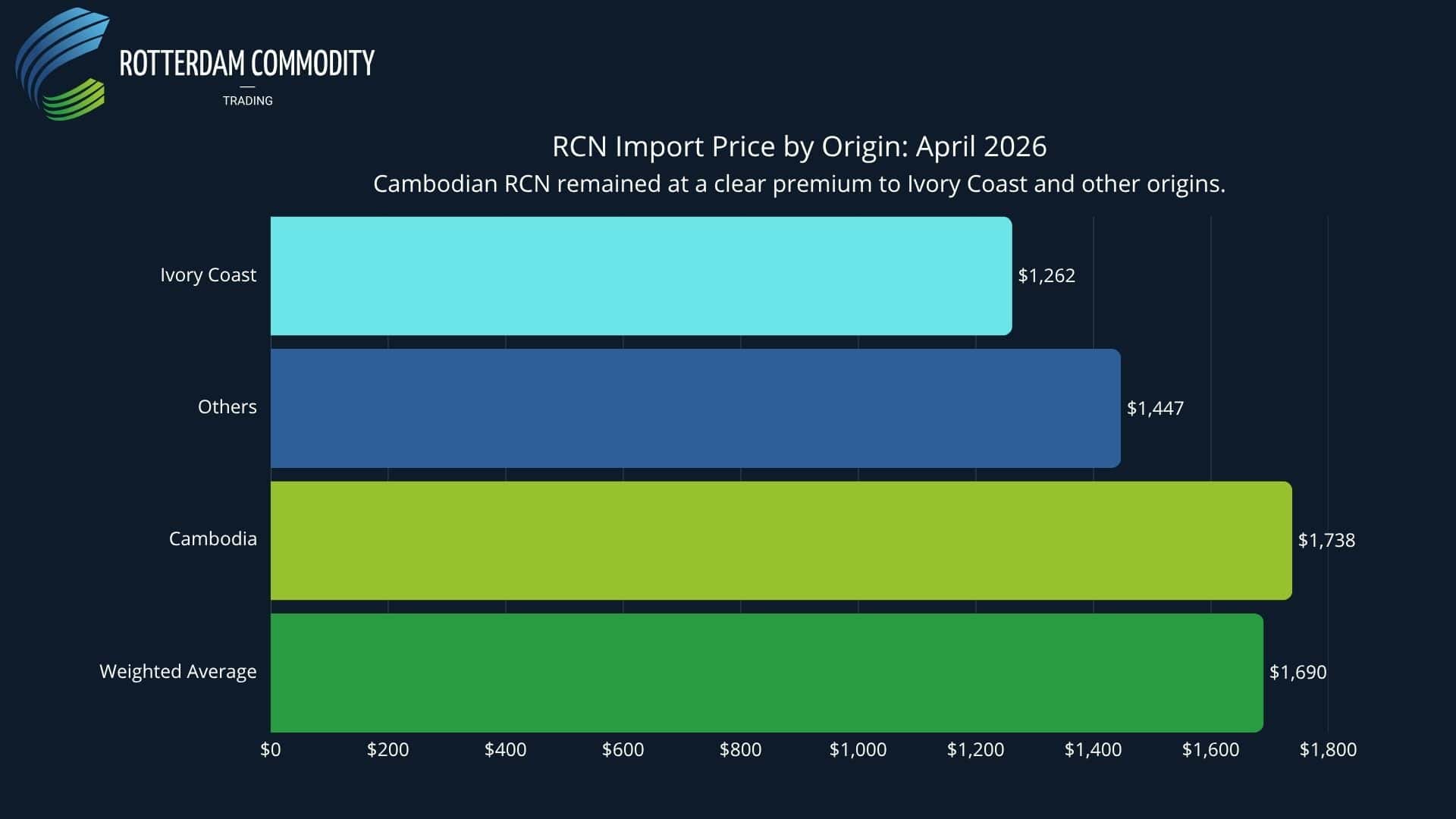

Import Prices: Cambodia Premium Keeps the Cost Base Elevated

The average RCN import price in April was USD 1,690 per ton, up 11.7% year-on-year and slightly above March’s USD 1,669 per ton. The cumulative January-April average was USD 1,618 per ton, almost flat year-on-year but 24.4% above VINACAS’s full-year plan price of USD 1,300 per ton.

The reason is again the origin mix. Cambodian RCN averaged USD 1,738 per ton in April. Ivory Coast averaged only USD 1,262 per ton, while other origins averaged USD 1,447 per ton. When Cambodia accounts for more than 86% of monthly supply, the headline import price is pulled toward the Cambodian premium.

This is not simply a question of price per ton. VINACAS again highlights the processing-efficiency issue for Cambodian raw material. Cargoes with 10–15% moisture require around 5.0–5.3 kg of RCN for 1 kg of exported kernels, while high-moisture fresh lots at 16–30% can require around 6.5 kg/kg. That makes the effective input cost more complicated than the headline import price alone suggests.

Ivory Coast remained the second-largest RCN supplier in April, but at a much smaller scale: 26,714 tons, or 4.9% of monthly imports. Mozambique followed closely with 25,024 tons, while Nigeria supplied 8,077 tons. Tanzania, which dominated the January off-season supply window and remained important in February and March, fell back to just 5,343 tons in April.

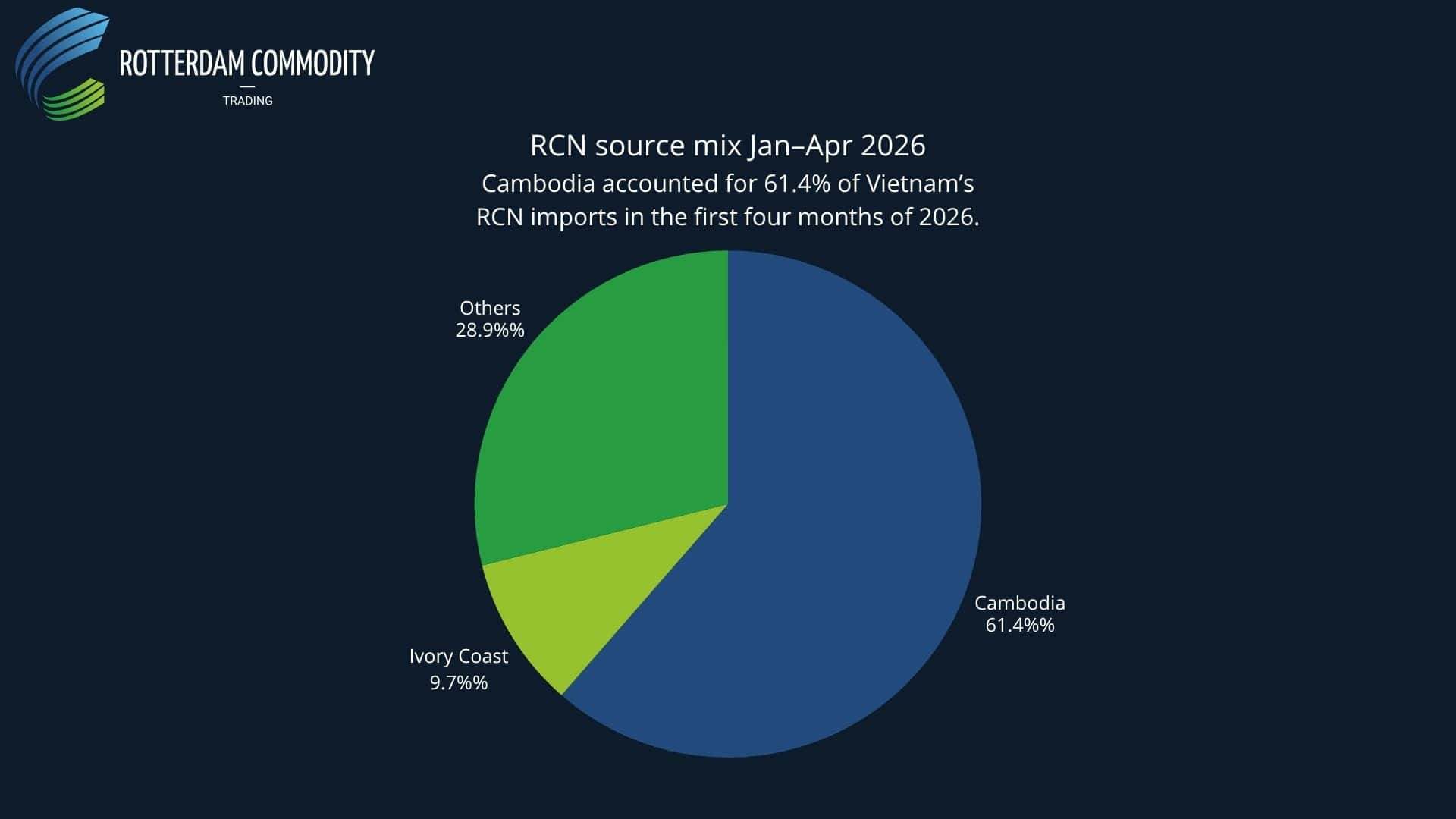

On a cumulative basis, Cambodia now accounts for 831,180 tons, or 61.4% of Vietnam’s total RCN imports in 2026 so far. Ivory Coast accounts for 9.7%, while other origins together make up 28.9%.

Borma Imports: Still a Structural Part of the Pipeline

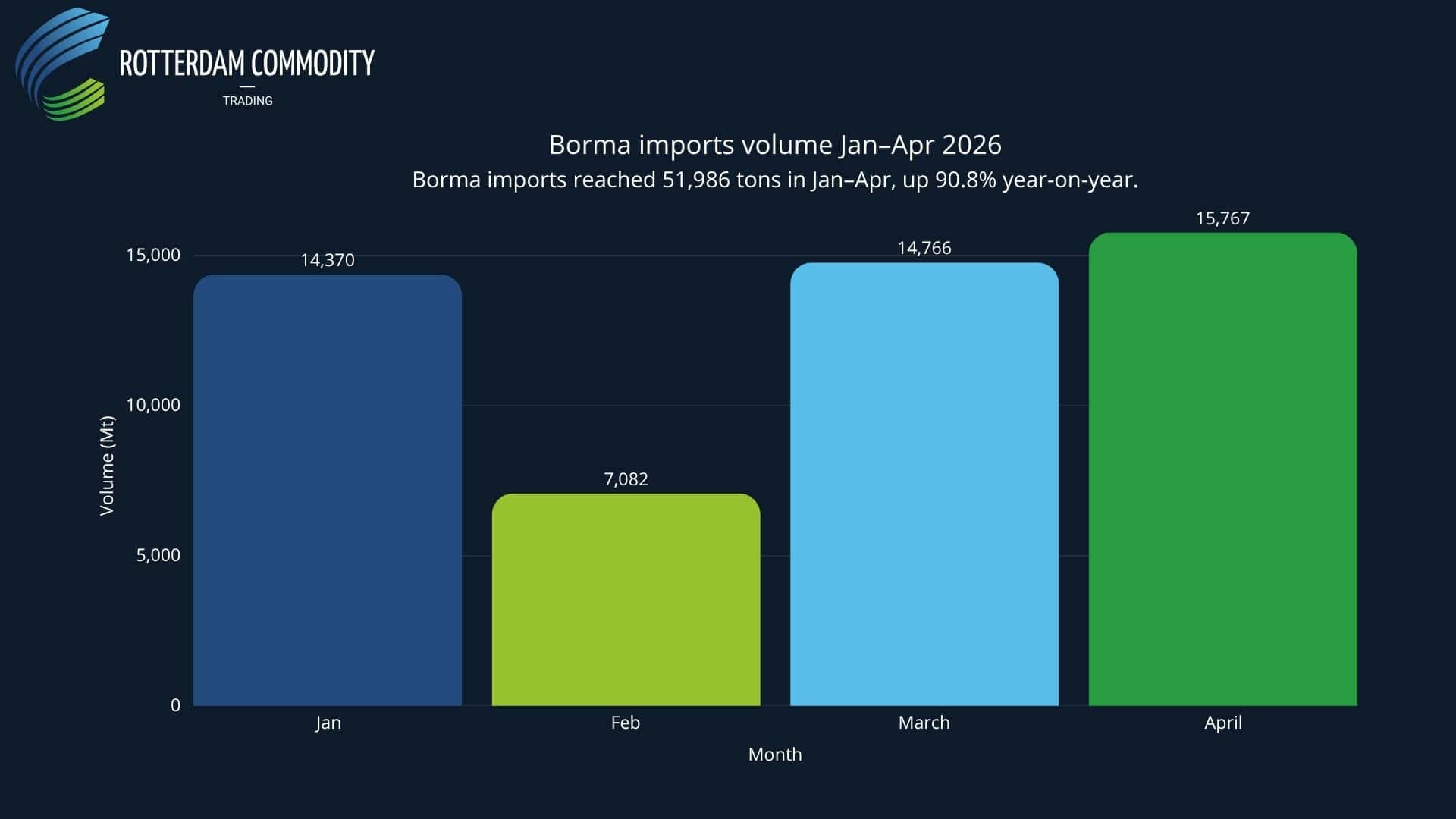

Imported borma cashews and white kernels also remained elevated. Vietnam imported 15,767 tons in April, up 105.3% year-on-year, at a value of USD 102.4 million. The average price was USD 6,497 per ton, down 5.0% year-on-year.

Across January to April, borma and white kernel imports reached 51,986 tons, up 90.8% year-on-year, with value up 81.1% to USD 328.0 million. When converted into RCN equivalent, imported kernels represented 13.9% of Vietnam’s total raw material inflow for the year so far.

That is lower than the January share, when borma imports played an especially large role during Cambodia’s seasonal absence, but it remains meaningful. Even with Cambodian RCN now flooding the pipeline, imported semi-processed material has not disappeared. It continues to function as a structural component of Vietnam’s processing model.

What April Means for the Market

April confirms that Vietnam’s cashew sector is operating at high speed. Export volumes reached their strongest monthly level of 2026, cumulative exports are comfortably ahead of last year, and raw nut imports are more than sufficient in headline terms.

But the market is not simply bullish. The key issue is balance. Cambodia is supplying Vietnam at scale, but at a premium to African origins. WW320 FOB prices continue to soften, even while the broader average export price improved. Borma imports remain high, but with a large unknown-origin share. China is back as the largest monthly destination, but cumulative Chinese volume is still below last year. The U.S., by contrast, remains the more consistent growth market.

For Q2, three variables matter most.

First, whether Cambodia can sustain the April pace without creating additional quality or moisture-related pressure. Second, whether China’s April return develops into sustained volume growth or remains a price-led recovery. Third, whether WW320 FOB prices can stabilise after four consecutive monthly declines.

The bottom line is clear: Vietnam has supply, it has export momentum, and it has demand across multiple destinations. What it still needs is a stronger margin signal. For now, the sector is winning on volume. Whether it can win on profitability will be the key question for the months ahead.

For weekly monitoring of Vietnam, Cambodia, West Africa and global cashew flows, including weather risk, yield signals and trade dynamics, subscribe to our cashew market updates.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.