Vietnam’s cashew sector entered February with a different character than its explosive January opening. The latest VINACAS figures show a market in recalibration: kernel exports dipped sharply compared to January’s surge, Cambodia returned to the supply picture in force, and the sourcing map shifted significantly as West African origins continued to ramp up volumes ahead of their main season.

February’s data is not a reversal of the 2026 story, on a cumulative January-February basis, the sector remains comfortably ahead of last year. But the month-on-month contrast is sharp enough to require careful reading. Export volumes fell 54% from January to February, a drop that is partly seasonal and partly reflective of the structural reality that January was an unusually strong month driven by pre-Lunar New Year procurement in China and inventory rebuilding elsewhere.

The more important February development is the return of Cambodia. After its near-total absence in January, Cambodia surged to become the second-largest RCN supplier in February, shipping 56,240 tons, a signal that the 2026 Cambodian season is underway. How that season develops over the coming months will be the defining variable for Vietnam’s processing margins and export capacity through mid-year.

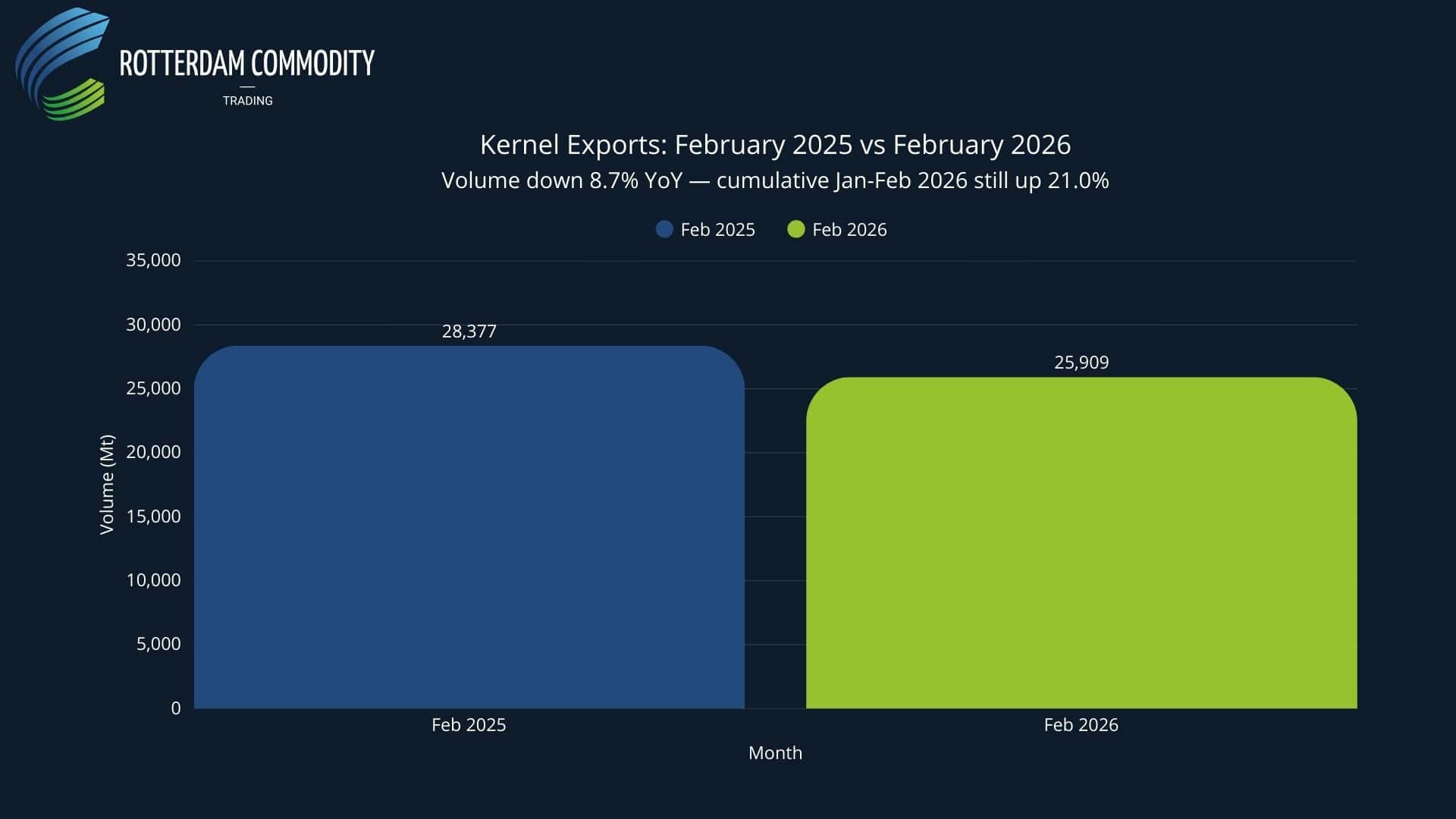

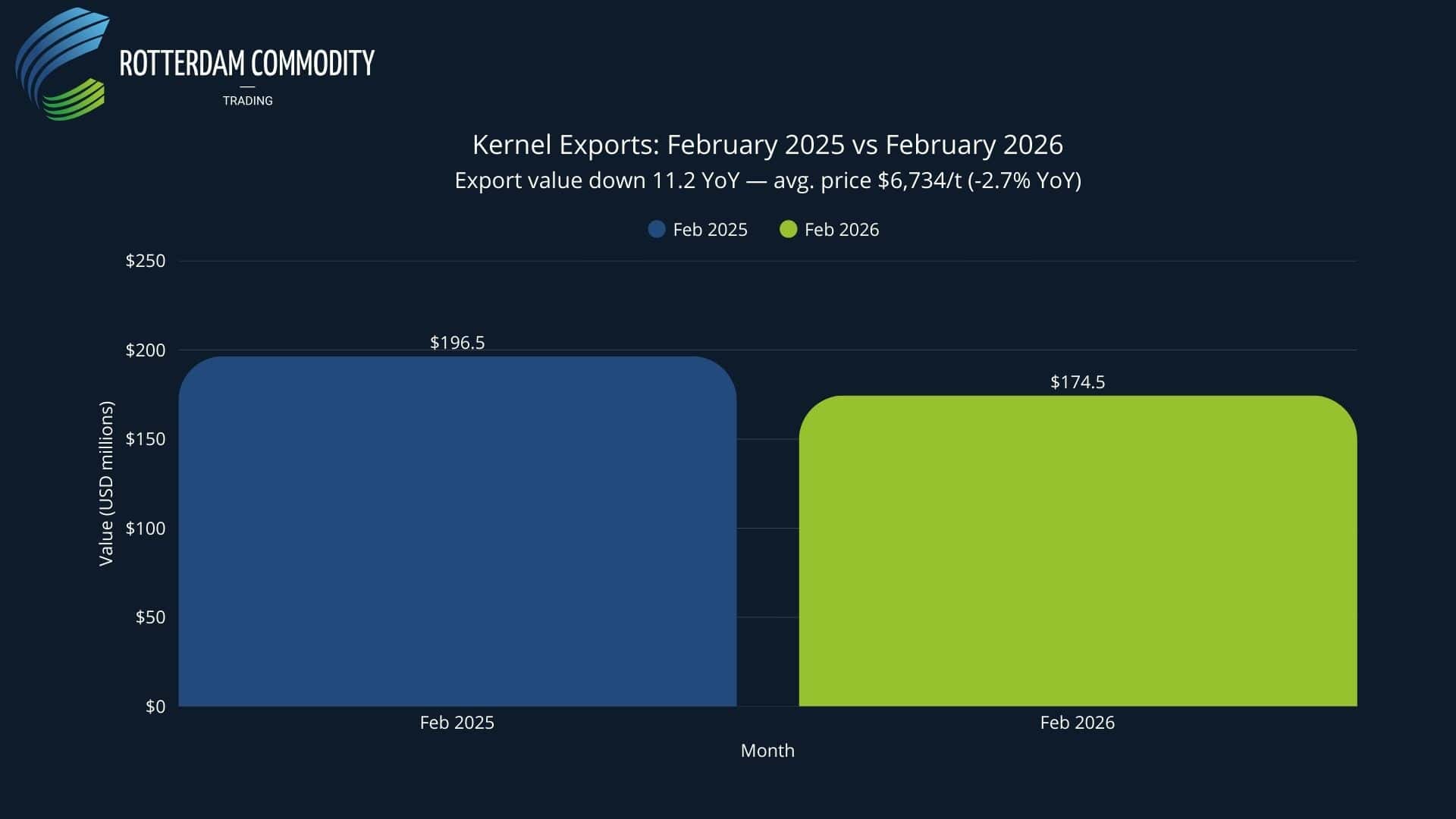

Kernel Exports: A Strong Month Still, But the Pace Eases

Vietnam exported 25,909 metric tons of semi-processed cashew kernels in February 2026, down 8.7% year-on-year versus February 2025. Export turnover fell 11.2% to USD 174.5 million, with the average export price at USD 6,734 per ton, down 2.7% YoY.

Read in isolation, these numbers look soft. But February 2025 was itself a strong comparison month, and the cumulative January–February picture remains firmly positive: 82,284 tons exported at USD 560.6 million, up 21.0% in volume and 19.8% in value year-on-year. The two-month average export price of USD 6,792/ton is down just 1.3% from the same period in 2025, a modest compression that has so far been offset by volume growth.

The WW320 benchmark traded between USD 3.15 and USD 3.88 per pound FOB Vietnam in February, averaging USD 3.51/lb, up 2.2% year-on-year but notably softer than January’s USD 3.67/lb average. The spread between the highest and lowest FOB price in the month narrowed to USD 0.73/lb, compared to USD 1.05/lb in January, suggesting slightly more homogeneous contract pricing across the exporter base. VINACAS notes that FDI-linked processors continued to transact at the lower end of the range.

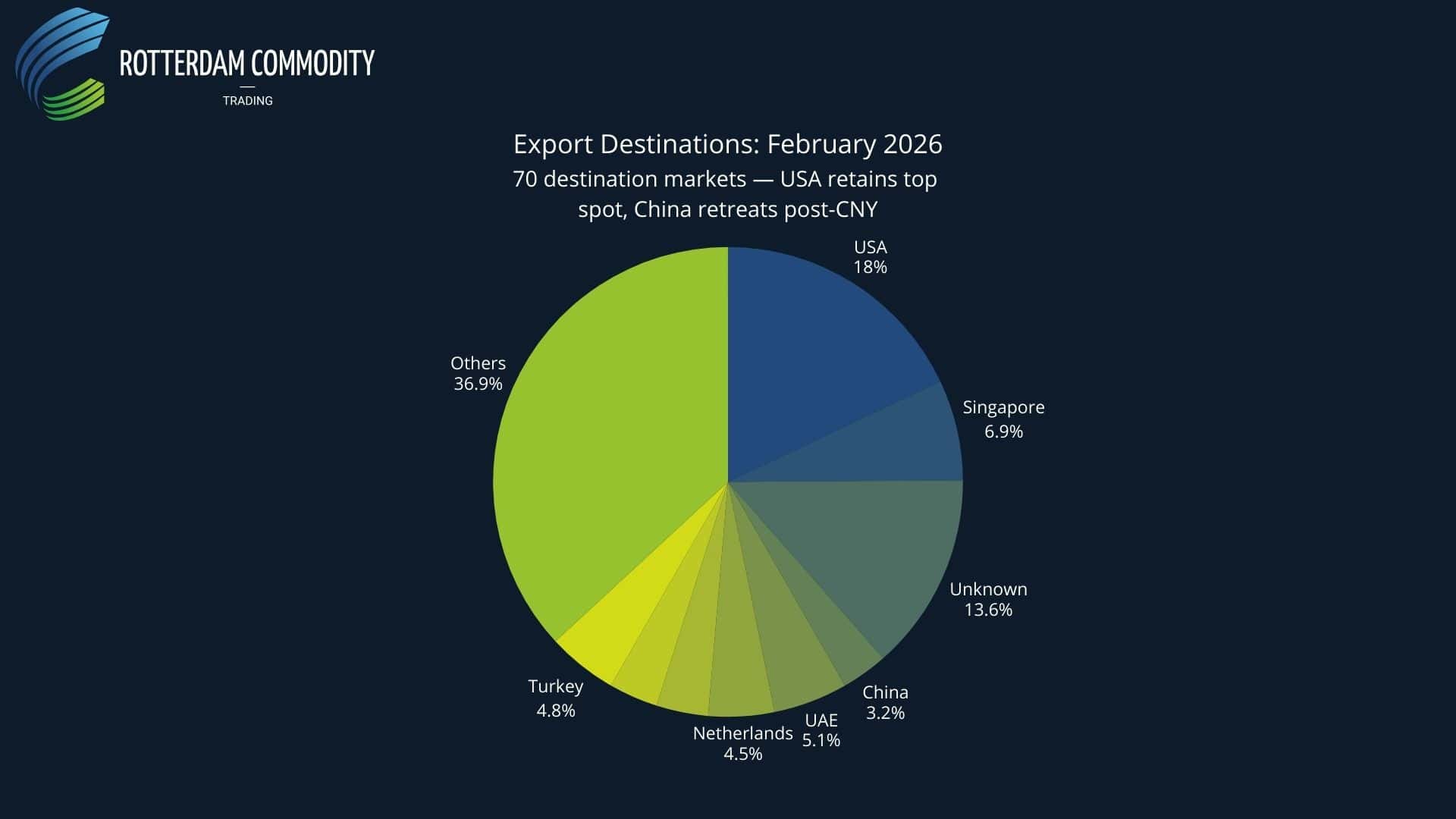

Export Destinations: U.S. Leads Again, China Retreats After Lunar New Year

The destination breakdown for February reflects the expected post-Lunar New Year slowdown in Chinese procurement and continued strength in Western markets.

The United States retained the top position with 4,822 tons (18.6% share), up 25.5% year-on-year in volume and 25.2% in value. On a cumulative basis, U.S. shipments reached 14,485 tons across January–February, up 30.0% YoY, one of the strongest bilateral trade performances for any single destination. This sustained pace suggests structural restocking rather than a one-month anomaly.

China dropped sharply to 845 tons (3.3% share), ranked 8th by destination, down 77.8% year-on-year. This is almost entirely a calendar effect: February is when Chinese Lunar New Year falls, and domestic consumption absorbs most available cashews before buyers return to the market in March. The cumulative January–February figure of 7,050 tons remains up 14.3% YoY, anchored by January’s 6,205-ton surge.

Singapore ranked third at 1,871 tons (7.2%), while Turkey (1,285 t), UAE (1,369 t), Netherlands (1,222 t), and United Kingdom (955 t) all registered solid volumes. The EU and other markets collectively absorbed 20,242 tons, roughly 78% of total exports, even in a softer month for overall volumes.

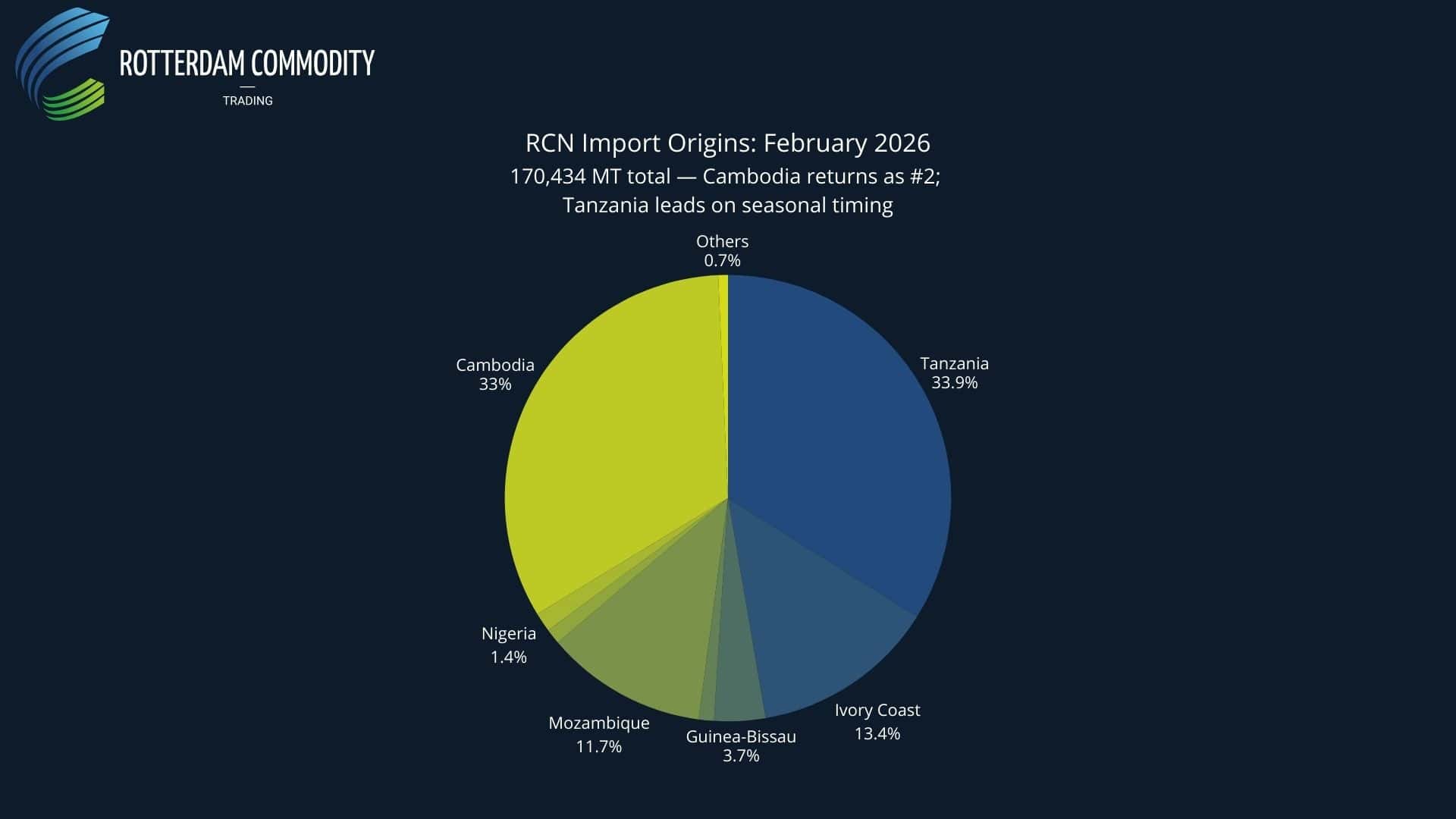

Raw Nut Imports: Cambodia Returns, Tanzania Still Leads

February’s RCN import data captures the transition the market has been anticipating since January: the return of Cambodian supply as the 2026 harvest begins. Vietnam imported 170,434 tons of raw cashew nuts in February, up 16.1% year-on-year, with total import value reaching USD 267.6 million (+7.7%). The average import price was USD 1,570/ton, down 7.2% from February 2025.

On a cumulative January–February basis, Vietnam has now imported 334,401 tons of RCN, up 25.1% year-on-year at a combined value of USD 520.4 million (+13.4%). The two-month average price of USD 1,556/ton is down 9.5% compared to the same period in 2025, a meaningful cost reduction for processors, though one that is partly offset by higher moisture content and lower outturn ratios in some African origins.

Tanzania retained the top position in February with 57,782 tons (33.9% share), making it the dominant supplier for a second consecutive month. Tanzania’s continued prominence reflects both the structural availability of East African supply during the inter-campaign period and the competitive pricing that Vietnamese processors have found attractive. On a combined January–February basis, Tanzania is Vietnam’s single largest RCN source.

Cambodia surged to second place at 56,240 tons (33.0% share), a dramatic reversal from January’s near-absence (771 tons). Year-on-year, Cambodia’s February volumes are up 47.5%, confirming that the 2026 harvest began early and at scale. This is the critical data point for supply chain planning across the sector: if Cambodia maintains this pace through March and April, total 2026 Cambodian supply to Vietnam could approach or exceed last year’s exceptional volumes. VINACAS notes that Cambodian RCN with moisture levels between 10–15% yields an RCN-to-kernel conversion ratio of 5.0–5.3 kg per kg exported, while higher-moisture fresh crop (16–30%) requires up to 6.5 kg/kg, a processing efficiency variable that matters significantly for margin calculations.

Ivory Coast ranked third at 22,851 tons (13.4%), up 403% YoY in February, though again, this dramatic year-on-year comparison reflects the near-collapse of Ivorian shipments in February 2025 rather than an exceptional supply surge this year. The new IVC marketing season opened in early 2026 and flows appear to be normalising after last year’s disrupted export pattern.

Mozambique made a notable appearance at 19,895 tons (11.7%), ranking fourth, a significant volume for a single month from this origin. Guinea-Bissau (6,363 t), Nigeria (2,313 t), Indonesia (1,952 t), and Guinea Conakry (1,936 t) rounded out the top origins, with a total of 15 countries supplying RCN in February.

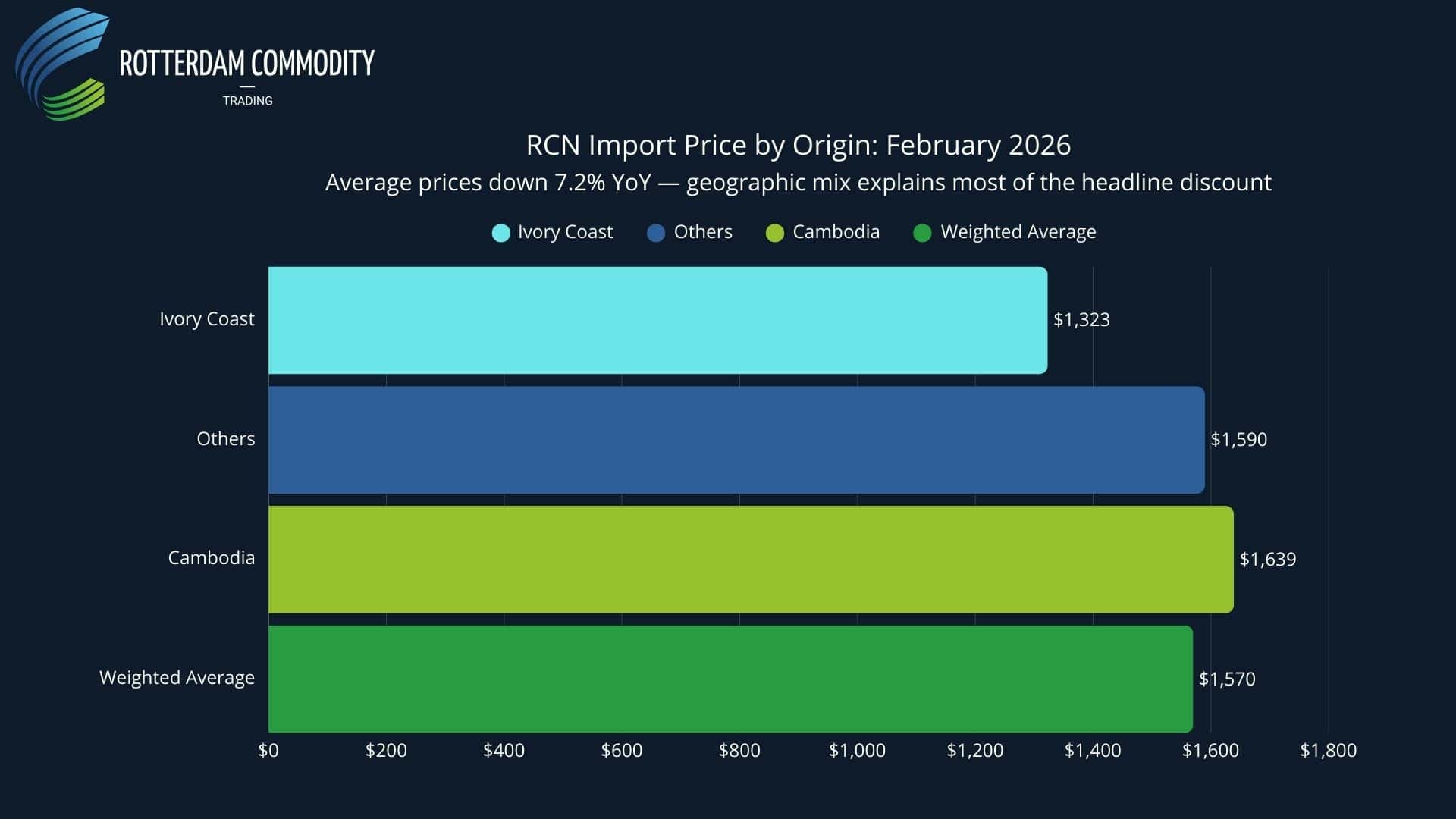

Import Prices: Geography Still Explains the Discount

The average RCN import price of USD 1,570/ton in February represents a 7.2% decline year-on-year. By origin, Ivory Coast averaged USD 1,323/ton (up 9.1% YoY, a reversal of January’s softness), Cambodia averaged USD 1,639/ton (down 1.6% YoY), and other markets averaged USD 1,590/ton (down 7.8% YoY).

The overall weighted average remains below both Cambodia and “other markets” because of the dominance of Tanzania and Ivory Coast, origins that historically trade at lower absolute price levels than Southeast Asian supply. This geographic mix effect continues to depress headline import prices relative to what processors actually pay for their preferred high-outturn, low-moisture Cambodian and East African premium material.

The cumulative two-month average of USD 1,556/ton is running approximately 19.7% above VINACAS’s full-year plan price of USD 1,300/ton. This gap between realised and planned import costs will be worth monitoring as the Cambodian season progresses and African origins reach full pace in Q2.

Borma Kernel Imports: Volume Normalises After January’s Surge

Imported cashew kernels in testa (borma cashews) and white kernels totaled 7,082 tons in February, up 30.1% year-on-year, at a total value of USD 42.7 million (+23.2%). The average import price was USD 6,026/ton, down 5.3% YoY, the second consecutive month of year-on-year price softness in this category.

February’s borma volumes are roughly half January’s 14,370 tons, a normalisation that likely reflects the beginning of the Cambodian fresh-crop season reducing the need for imported semi-processed material. On a combined basis, January–February borma imports reached 21,452 tons, up 72.3% year-on-year, a striking increase that underscores how important imported semi-processed material has become in Vietnam’s processing pipeline.

The Cumulative Picture: A Strong Start to 2026

Across both months, Vietnam’s cashew sector has delivered a strong opening to 2026. At USD 560.6 million in two-month kernel export value, the sector is tracking at 11.2% of VINACAS’s full-year export target of USD 5 billion, slightly ahead of the 10.3% pace implied by two months of a twelve-month year. The average export price of USD 6,792/ton is running at 108.7% of the annual plan price of USD 6,250/ton, providing a modest buffer for the months ahead.

On the import side, the sourcing strategy is working as intended: processors have secured 334,401 tons of RCN in the first two months, 10.45% of the full-year plan, at prices currently above target, but in an environment where supply availability has been broadly adequate.

What February’s Numbers Mean for the Months Ahead

February confirms several structural dynamics that will shape the rest of 2026:

Cambodia is back and running early. The 56,240-ton February import from Cambodia is the most important single data point in this month’s release. If the 2026 harvest maintains volume parity with 2025’s exceptional output, Vietnam’s processing pipeline will be adequately supplied through mid-year. If yields disappoint, the pressure on African origins to fill the gap will intensify, and at current African prices, the math on processing margins becomes more challenging.

Tanzania’s dominance. Tanzania topping Vietnam’s RCN import rankings in both January and February is consistent with its harvesting calendar: Tanzania has a minor season in January–February and a main season from October through December, making it one of the few origins with available fresh crop during the West African and Cambodian inter-campaign window. This is a reflection of seasonal timing, not a structural shift in the supply map. That said, Tanzania’s ability to fill the gap reliably during this window, and at competitive prices, does make it a practically important source during Q1. Its prominence will naturally recede once Cambodia hits full stride and West African volumes accelerate into Q2.

West African supply is accelerating. Ivory Coast, Guinea-Bissau, Mozambique, and Nigeria are all increasing shipments ahead of their main campaign seasons. By April and May, these origins will reach peak flow simultaneously with Cambodia, creating the potential for a supply-heavy Q2 that could put further downward pressure on RCN import prices and, indirectly, on kernel export prices if processors pass through cost relief in their FOB offers.

Export price resilience is the key variable. February’s WW320 average of USD 3.51/lb remains above year-ago levels (+2.2%), but the trend from January’s USD 3.67/lb is downward. If Cambodia’s season delivers abundant supply and African origins simultaneously run at full capacity, the pressure on kernel export prices could increase materially in Q2. Processors currently working on thin margins will need either firmer FOB prices or a continued volume advantage to protect profitability.

Weather risk is emerging as a material variable for Q2 supply. Unseasonal rainfall in Vietnam’s main cashew-growing regions during the critical flowering and fruit-set window in early March poses a direct risk to Vietnam’s domestic crop yield. Simultaneously, unusual humidity in Ivory Coast during harvest is threatening RCN quality and delaying farmgate deliveries. Early price signals in the Vietnam-Cambodia corridor are already reflecting these concerns, with RCN hovering around VND 55,000/kg (~$2,090–2,100/PMT). If these weather patterns persist, the supply-heavy Q2 scenario described above may not materialise, and processors may instead face tighter supply and firmer RCN prices precisely when export demand is at its seasonal peak. For a detailed analysis of the crop signals, see our separate report: “Unseasonal Rainfall and Atmospheric Anomalies Threaten Global Cashew Supply as Vietnam and Ivory Coast Crop Signals Weaken“

The Bottom Line

February 2026 is a month of transition. Cambodia has returned to the supply map, West Africa is ramping up, and Vietnam’s export machine is running at a sustainable, if slightly more modest, pace after January’s exceptional volume. The cumulative two-month picture remains solidly positive, and the sector is on track against its full-year targets.

But the coming weeks are when the 2026 story truly begins to take shape. Cambodia’s harvest depth, Ivory Coast’s total exportable surplus once its domestic processing sector takes its share, and the trajectory of WW320 prices as supply builds, these will determine whether Vietnam’s cashew sector can translate a strong early start into a genuinely strong full year.

The machine is running. The supply is arriving. The question, as always, is whether the price will hold and whether the weather will cooperate. With unseasonal rainfall already impacting Vietnam’s domestic flowering season and Ivory Coast’s harvest quality under pressure, that second question is no longer hypothetical.

For weekly monitoring of Vietnam, Cambodia, West Africa, and global cashew flows, including weather risk, yield signals, and trade dynamics; subscribe to our updates.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.

We use cookies to ensure you get the best experience on our website. For more information, please read our Privacy Policy.